'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

In the previous post, we discussed how using a Variable Prepaid Forward (VPF) contract can help investors looking to use highly appreciated stock to cover their large upcoming expenses. It could be buying a property, starting a new business or gifting assets to heirs. We are talking about $1M+ transactions.

A VPF reduces downside risk relative to simply holding the appreciated stock and using a Securities-Based Line of Credit (SBLOC) and allows delaying the payment of capital gain taxes. You can learn why delaying realizing capital gains is important here.

At the same time, VPF should be considered as a riskier strategy than simply selling the stock today to cover the large expense. If the stock doesn’t grow in the next N years (the duration of the VPF contract), the investor loses money equal to the VPF discount (normally 15-20%).

VPF Contracts as a Diversification Tool

But what happens if the investor enters into a VPF contract, but instead of using the money received from the bank to cover their upcoming expenses, they invest the proceeds? How much investment risk do they actually take?

It turns out that in this case the VPF contract acts as leverage: the investor continues to own the concentrated stock for the next N years, and at the same time they are also invested in the market. It could be a simple total stock market fund or more aggressive Long/Short direct indexing strategy, but the important thing is that they are invested twice:

Concentrated Stock: investment risk is limited by Floor, upside is limited by Cap

Diversified Portfolio: No Floor and Cap but portfolio is diversified

The investor should know that during the VPF contract they are taking more investment risk in their portfolio. Depending on their financial goals (their future expenses) and their current savings, exposing themselves to additional investment risk may be either a good or bad idea.

When estimating potential benefits of using the VPF contract as a diversification tool, the investor needs to take into account not only the expected return of concentrated stock but also expected return of the diversified portfolio. These two may or may not move in the same direction and it significantly impacts the benefit of the strategy:

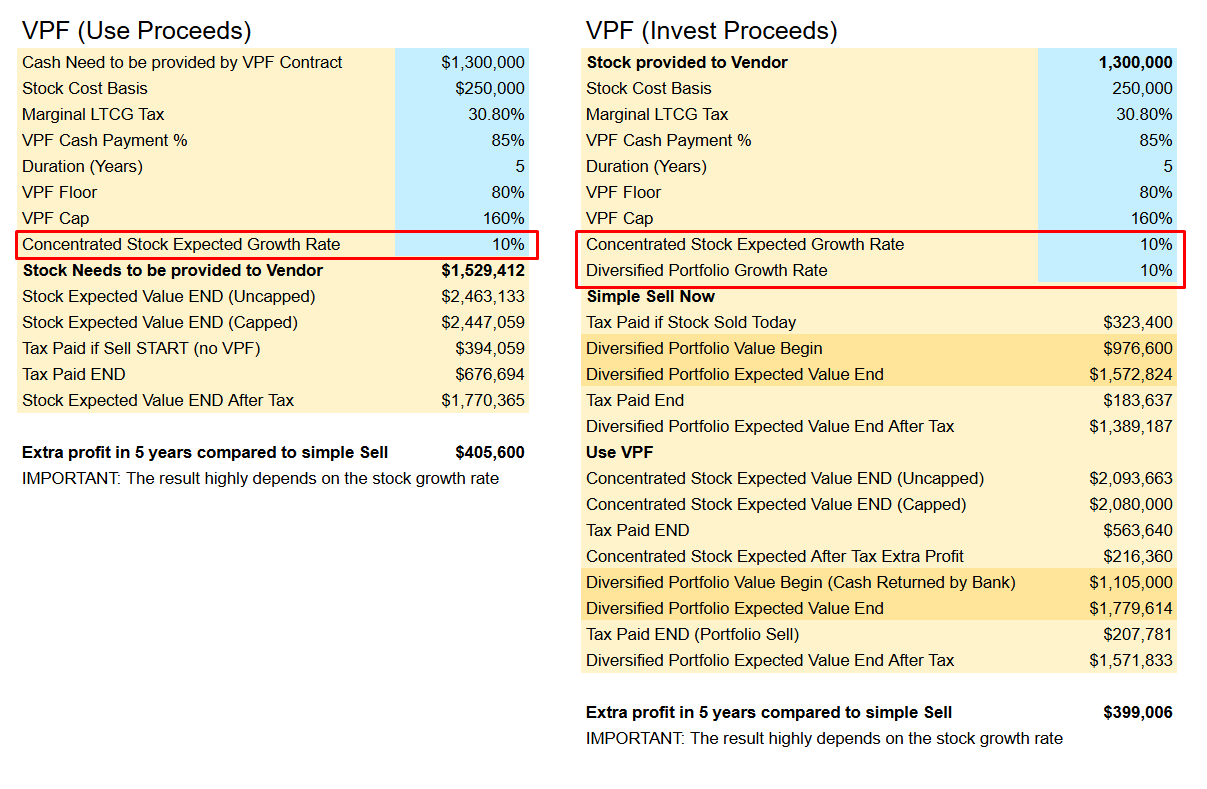

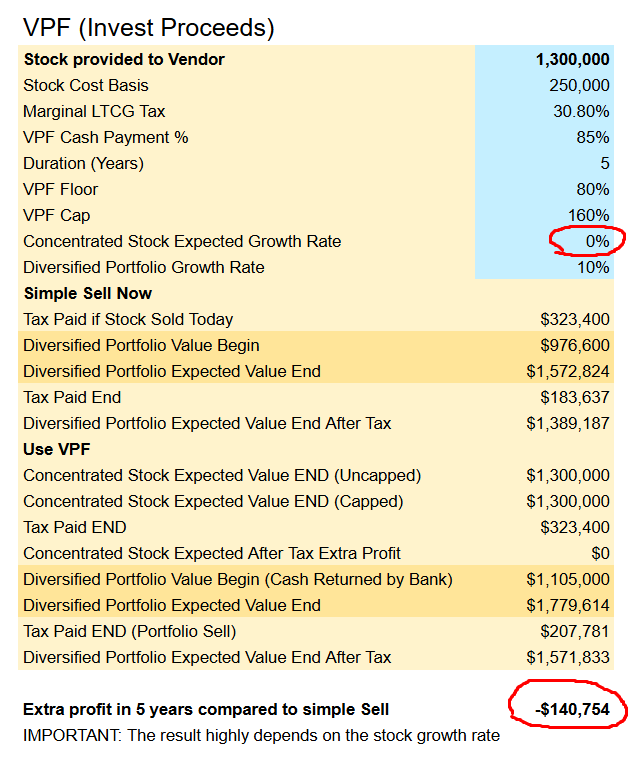

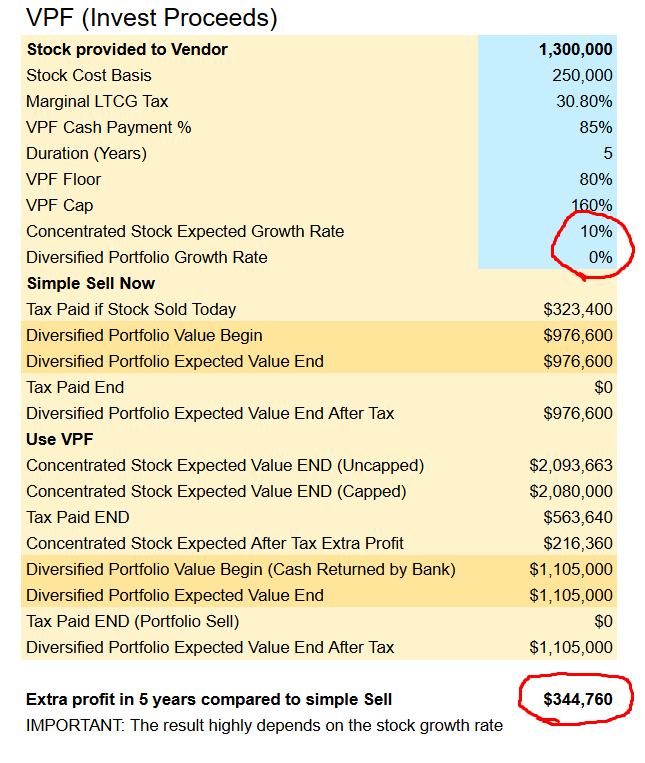

The investor makes money using a VPF contract only when the concentrated stock is expected to grow. If the stock remains flat or drops significantly in the next N years, the investor loses money equal to VPF discount minus diversified portfolio return. Consider this example:

Stock Provided to Bank = $1.3M

Cost Basis = $250K

VPF Cash Payment = 85%

if the concentrated stock does not grow (0%), but diversified portfolio generated 10% annually, the total loss is $1.3M x 15% - $54.2K = $140.7K, where

$1.3M x 15% = VPF fees

$54.2K = 10% annual return generated by diversified portfolio over 5 years

What is the best use case for VPF?

Using this strategy makes sense when the investor thinks that the concentrated stock will continue to go up in the next N years (duration of the VPF contract), but they can’t accept the amount of risk that comes with holding this individual stock. There are two components when it comes to risk management

Risk tolerance - how much risk the investor is comfortable taking emotionally (psychology).

Risk capacity - how much risk the investor can afford to take financially (financial goals).

For instance, if the investor has a net worth of $8.8M and for all of their financial goals they need $6M today, they can’t have a concentrated position of $4M. If this concentrated stock drops 90% and never recovers, it’ll affect the investor’s financial goals.

In the next example, if the concentrated stock appreciates 10% annually, but the diversified portfolio stays flat (0% annual return), the investor receives extra $344.7K profit after fees when using VPF compared to simply selling the stock today. Why? In the model the stock continues to appreciate 10% annually and money not paid as taxes continues to appreciate over the next 5 years.

Yes, the investor will pay more in taxes eventually ($563.6K 5 years from now instead of $323.4K today) but even with that they make more money.

Benefits, Investment Risk and Fees

When we make a decision about using a financial strategy or product, we need to understand all three aspects:

Expected Benefit

Investment Risk

Fees

VPF benefit depends on the current value and cost basis of the concentrated stock, marginal long term capital gain tax rate, expected return of the concentrated stock in the next N years and parameters of the VPF contract (floor, cap, duration and cash payment). A simple deterministic model to estimate the benefit can be built in Google Spreadsheets by comparing two scenarios:

Simply sell the concentrated stock today and pay taxes

Use VPF contract and pay taxes N years from now when delivering the stock

In contrast to most other financial products, VPF contract fees are the easiest to calculate: it’s the difference between the current stock value and cash payment you receive in return today from the bank. The 15-20% discount represents the fees. The fees are determined by the duration of the contract and interest rates.

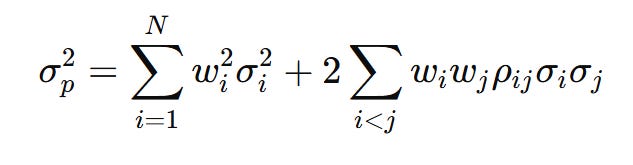

Calculating the investment risk is the hardest part when making a decision to use VPF contracts in the portfolio. During the contract (N years) the investment risk is elevated, because the VPF contract acts as leverage and the portfolio contains approximately 54% concentrated stock and 46% diversified portfolio (only 85% of current concentrated stock is delivered by the bank as a payment and then invested in a diversified portfolio).

There is a formula to calculate the overall portfolio volatility (measure of investment risk) for N:

where,

w[i] = weight of stock i

sigma[i] = standard deviation of stock i

ρ[i,j] = correlation between stock i and stock j

The challenge is that by setting Floor and Cap for the concentrated stock we affect both standard deviation of the stock and its correlation with other stocks in the portfolio. The right (and simplest) approach would be to run Monte Carlo simulation with Cap and Floor, and it’s a topic for a separate blog post.

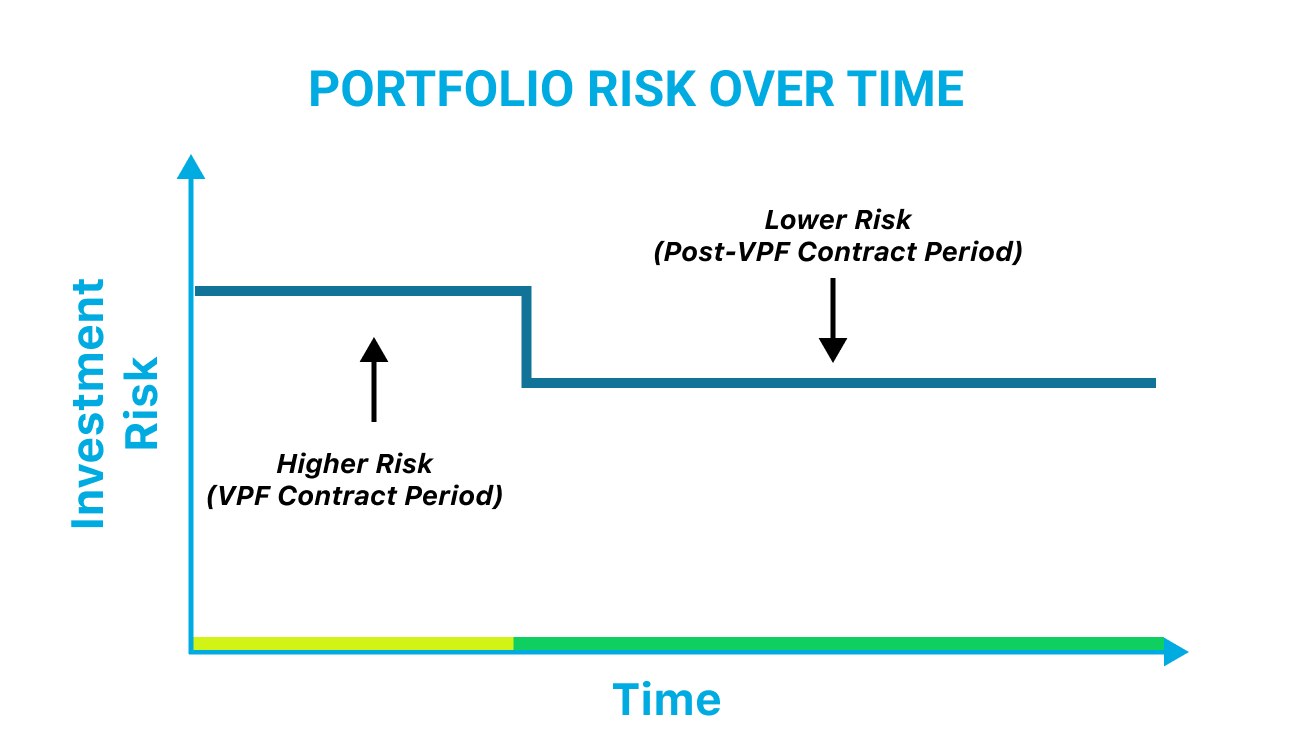

To get started, the investor should know that their investment risk (standard deviation) in the portfolio is higher during the VPF contact:

Conclusion

The Variable Prepaid Forward (VPF) contract is a sophisticated financial instrument which could be used by investors managing concentrated, highly appreciated stock positions. It enables the transition toward a diversified portfolio while deferring the significant capital gains taxes.

The Tax Arbitrage: The primary “win” is keeping money that would have gone to the IRS working for you for an additional $N$ years. If your diversified portfolio or the concentrated stock performs well, the compounding effect on those deferred taxes can be substantial.The Leverage

Leverage: VPF isn’t just a hedge, it’s a form of leverage. By reinvesting the proceeds while still holding the capped/floored stock, you are effectively “double-exposed.” This is why understanding your Risk Capacity (how much you can afford to lose without ruining your goals) is important as well as your emotional risk tolerance.

The Growth Prerequisite: A VPF is rarely a winning strategy for a stock you expect to stagnate. Because of the 15-20% fee, you generally need the concentrated stock to appreciate or the diversified portfolio to significantly outperform the cost of the contract to break even.

About the Author: Alex Sukhanov, founder of Nauma, a financial planning platform built for people in tech and high-net-worth families. Alex previously worked at Google and started Nauma to help more people in tech make better financial decisions and achieve more in their lives. You can reach out to Alex on linkedin.

Nauma is supported entirely by its users with no commissions and no affiliate incentives. It is designed to give people clarity on taxes, equity compensation and retirement planning.