'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

The challenge with using swap (exchange) funds is that the highest demand happens during booms like the one we experience today: successful company’ stocks appreciate to levels that make many employees uncomfortable having their wealth concentrated in one name. But the benefit of using exchange funds highly depends on the expected stock market returns, which are normally lower over the next 5-15 years after a boom.

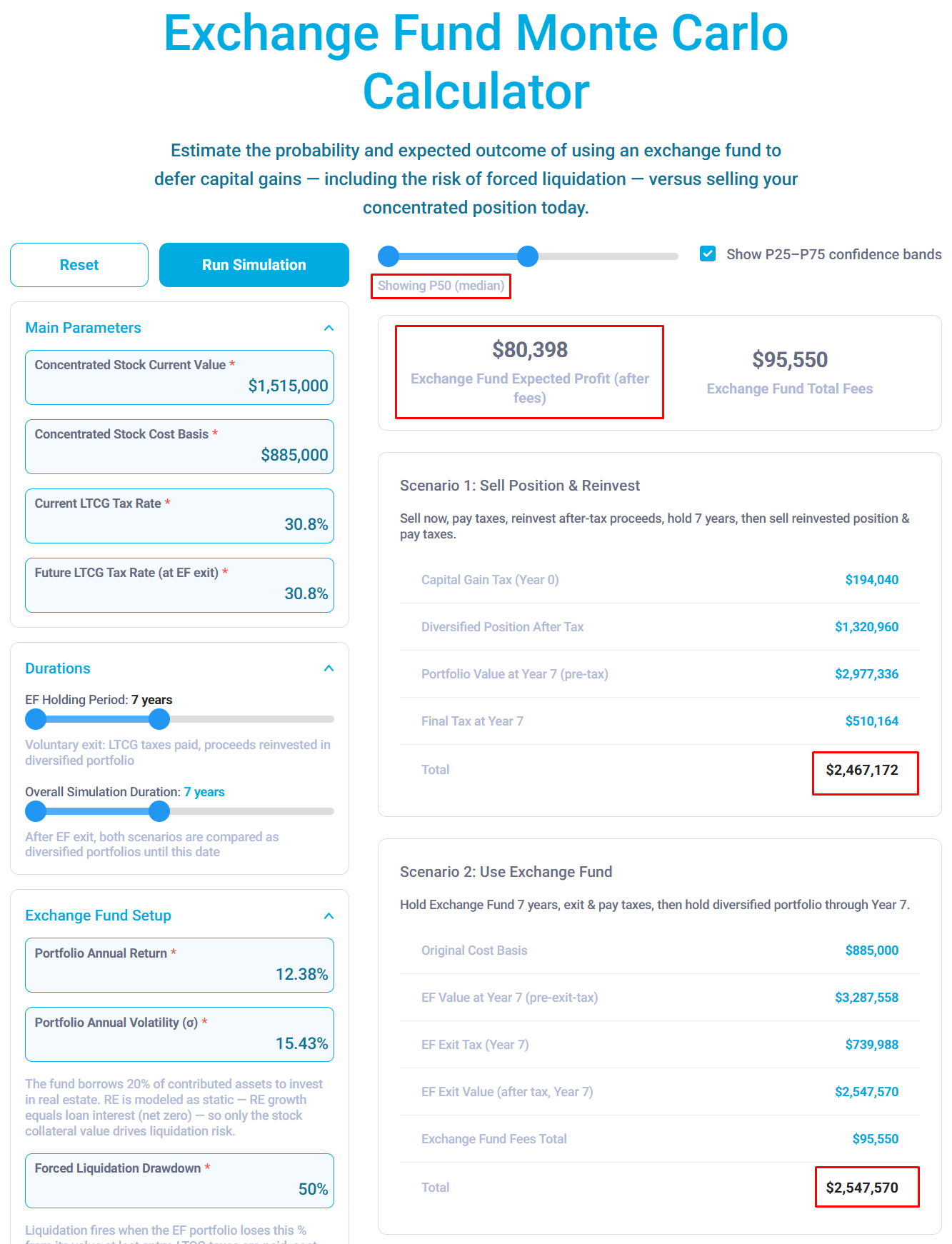

Consider an example: concentrated stock value = $1.5M, cost basis = $885K, current and future LTCG tax rate are expected to be the same = 30.8% (20% federal + 3.8% NIIT + 7% WA State). Expected Market Return = 12.38%, expected Volatility = 15.43% (S&P 500). Duration = 7 years (standard IRS requirement)

We consider two scenarios:

Exchange fund: the investor uses an exchange fund, waits seven years, and then sells everything to get cash.

Simple sell: the investor sells the stock now, invests in a diversified portfolio, waits seven years, and then sells again.

We finish both scenarios with a full liquidation to make them comparable.

Monte Carlo P50 (median market returns) gives us:

Simple Sell Scenario = $2.46M

Exchange Fund = $2.54M

Exchange Fund Benefit = $80K

Monte Carlo P5 (Pessimistic Market Returns) gives us:

Simple Sell Scenario = $1.46M

Exchange Fund = $1.43M

Exchange Fund Benefit = -$28K

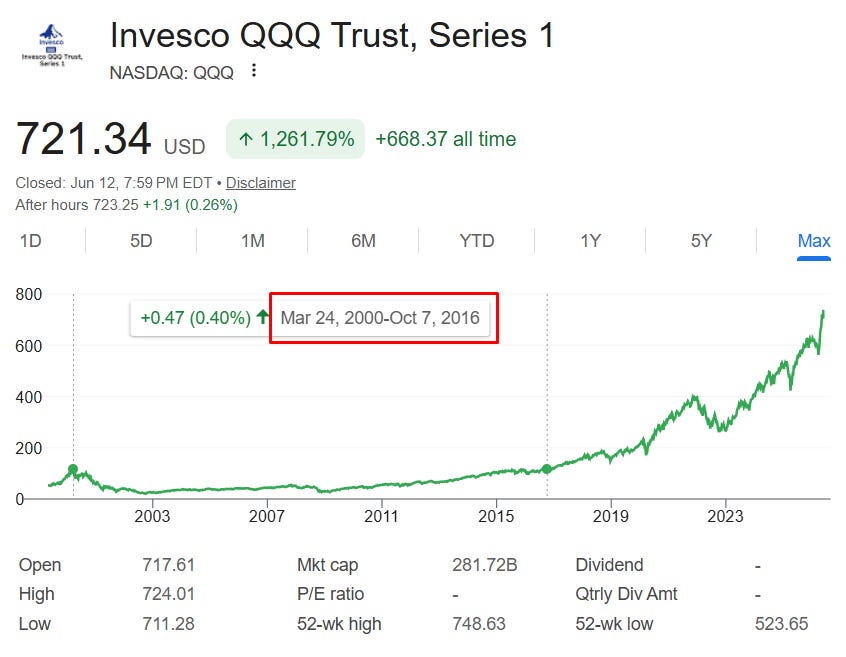

Between 2000 and 2016, QQQ remained flat, with a 0% return. Today, the Shiller P/E ratio, or cyclically adjusted price-to-earnings ratio, is at a level comparable to the dot-com bubble, which makes some people believe that investment returns will be lower over the next five to ten years.

At that level of return, exchange funds may add very little value compared to simply selling.

With all that said, there is a problem with this thinking: by adding the sell step at the end of the seven-year period to make both scenarios comparable, we oversimplify the problem. In reality, people who use exchange funds get optionality: they can continue to manage that position and diversify without triggering taxes in the future, especially if they stop working during that period and gain access to the 0% LTCG tax bracket. People who sell appreciated stock today don’t have that privilege: they lock in their gains and pay the taxes today.

Tax-efficient diversification is not a one-time solution, but a multi-year process.