'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Families who have a financial plan in place experience less stress if they are affected by layoffs. Understanding their financial situation helps them think clearly and more broadly about their career and consider less traditional paths such as taking time to recharge, learning new skills and trying an idea they’ve always been thinking about.

Uncertainty and lack of understanding of the financial situation, on the other hand, push people without a plan to find another job as quickly as possible. In the challenging market like today (February 2026) it’s hard. The number of available well-paying and interesting positions is far less than the number of people looking to get them. High competition turns into a frustrating experience: days spent filling meaningless online applications and no interviews.

Layoffs are stressful and emotional. No matter how prepared someone is, it can still feel like rejection. Going through a prolonged job search in an extremely tough market can further erode confidence. This vulnerability makes it easy to fall into a trap: accepting any available job, even if it’s not well aligned with career goals and professional interests.

Taking a step back and reassessing the situation is a better approach.

What is a Financial Plan?

A good financial plan includes a list of family goals and the actions the family should take to achieve them with a desired probability. That’s it.

If a family can clearly articulate:

Their major upcoming life events (having kids, moving parents, buying a house, starting a company)

How much each life event will approximately cost (accounting for inflation)

How much they need to save today to cover those future costs

How much they should reserve for taxes, given how they use tax-advantaged accounts

The probability of success based on their portfolio and contribution/withdrawal schedule

…then they have a plan.

Otherwise, the family is operating blindly, and major unexpected events such as layoffs, a market crash, or an unexpected loss can create significant stress which potentially lead to reactive mistakes.

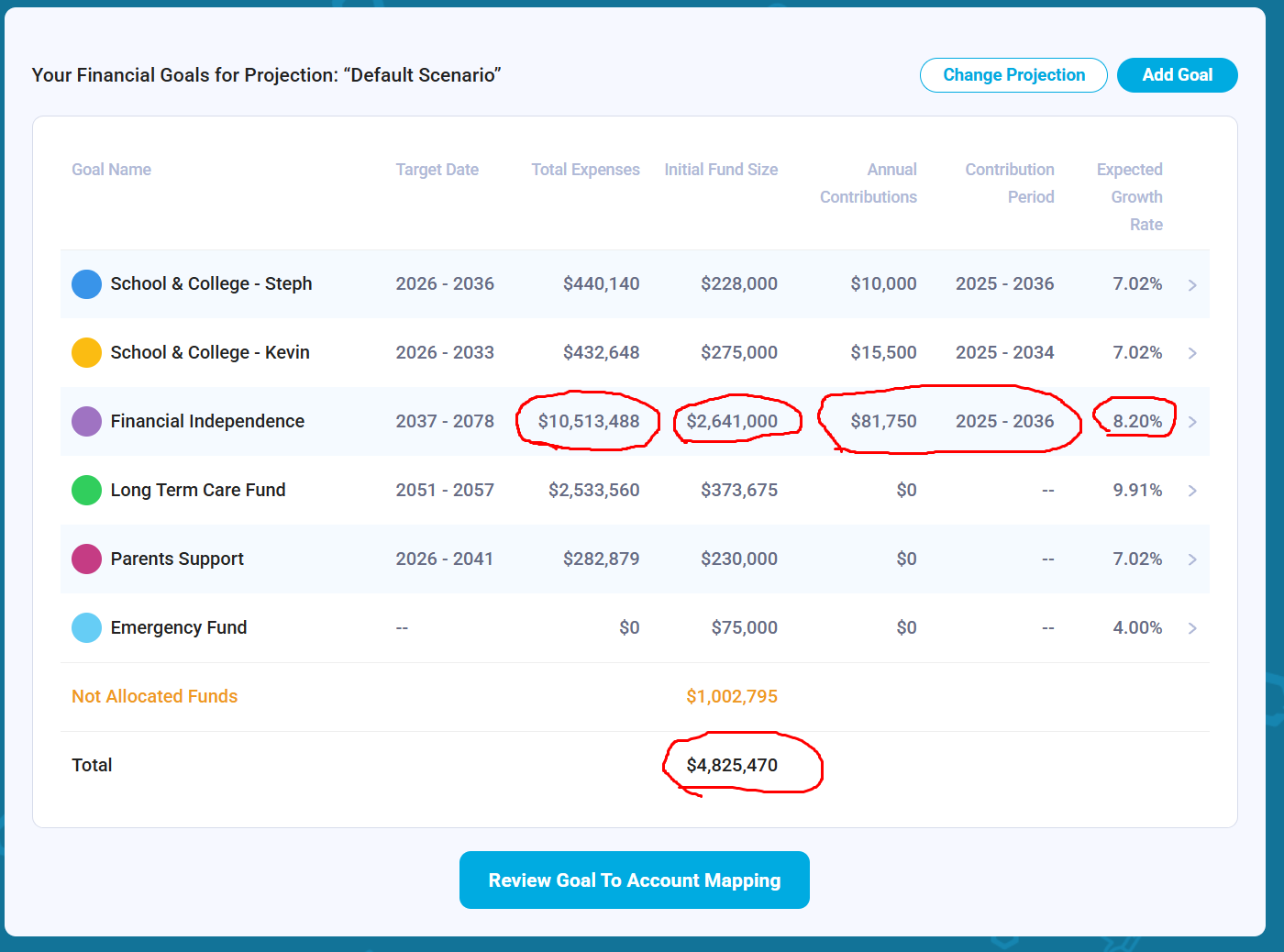

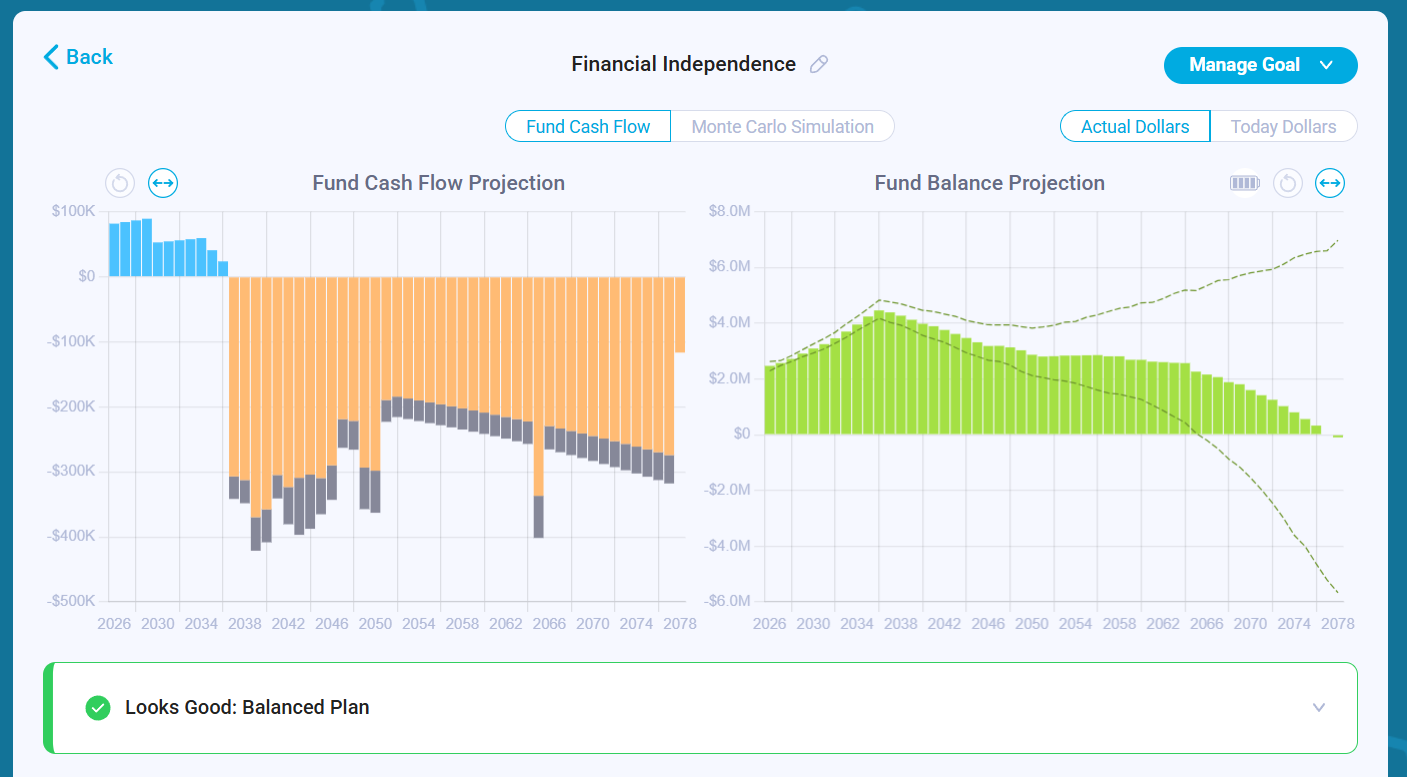

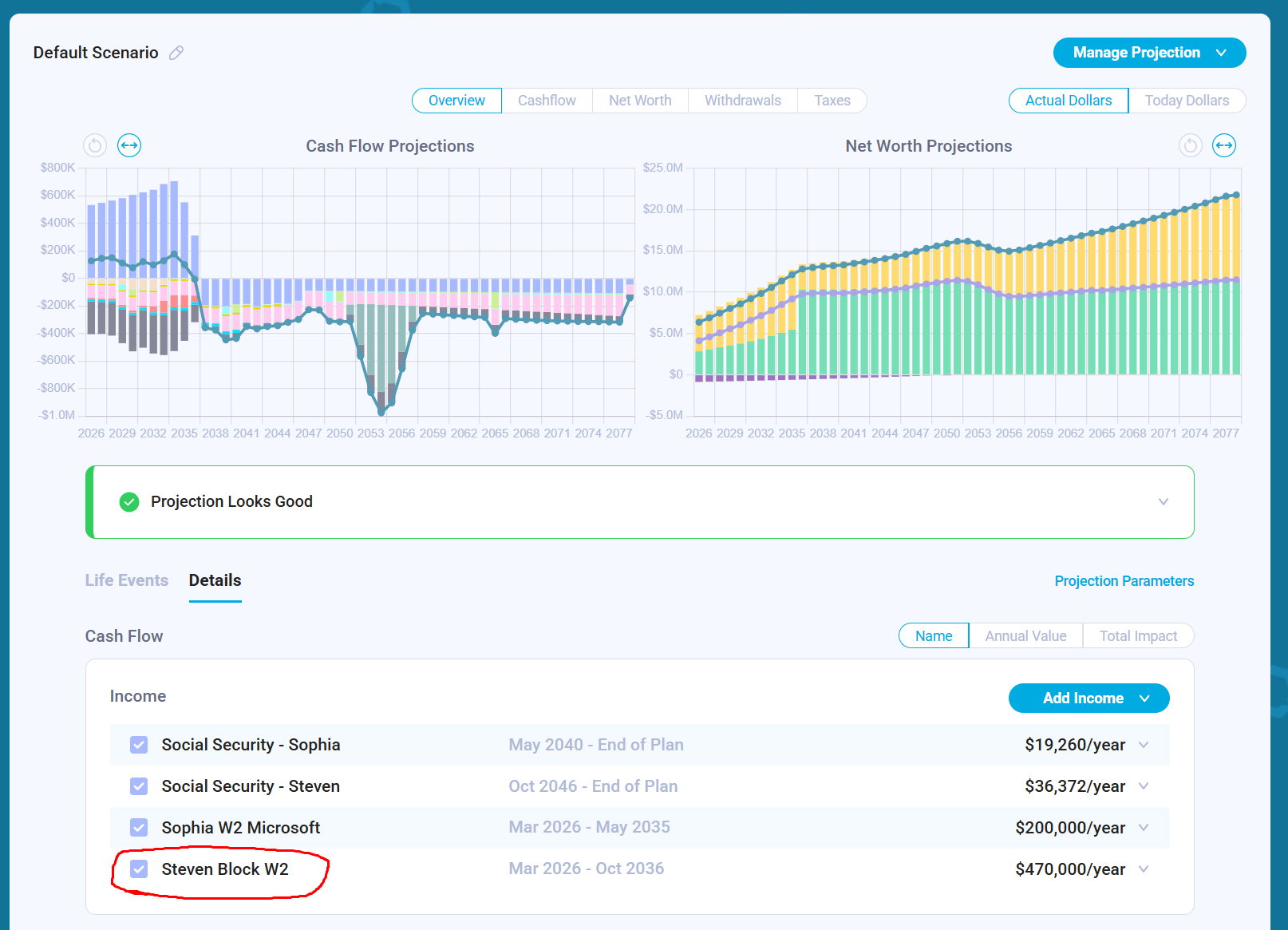

Consider an example: The family lives in California. Their net worth (excluding primary residence) is $4.8M. They estimate that their total expenses to cover their retirement needs are $10.5M. To cover these future expenses, they already allocated $2.6M from current savings and plan to maximize their retirement contributions until 2036. They are looking to get an 8.2% target return.

The family separated their other goals. They have two children who will go to college. They estimated that the total school & college expenses are around $440K per child and in order to cover these expenses the family needs to allocate $228K-$275K from their savings and then contribute 10K+15K = $25K/year.

They also have other goals which they can see on the dashboard. This family has a plan.

Are We Trying to Predict the Future?

Financial Planning is not an attempt to predict future life events, investment returns, inflation and taxes. Instead, it’s an attempt to articulate family preferences, making sure that these preferences are reasonable and then identifying steps that should be taken to achieve the things they want. Financial planning is about setting direction and being intentional about money.

Most assumptions about the future are wrong and mistakes tend to accumulate over time. That said, regular updates of the financial plan help mitigate that and adjust the trajectory based on the information received from the real world. This approach makes financial plans useful and helps see issues early before they become big problems for the family.

If the plan doesn’t hold anymore, the family adjusts their financial goals by either:

changing their income (staying employed longer or changing a job)

adjusting expenses

changing investment risk and expected return in the investment portfolio

Updating Income & Expenses

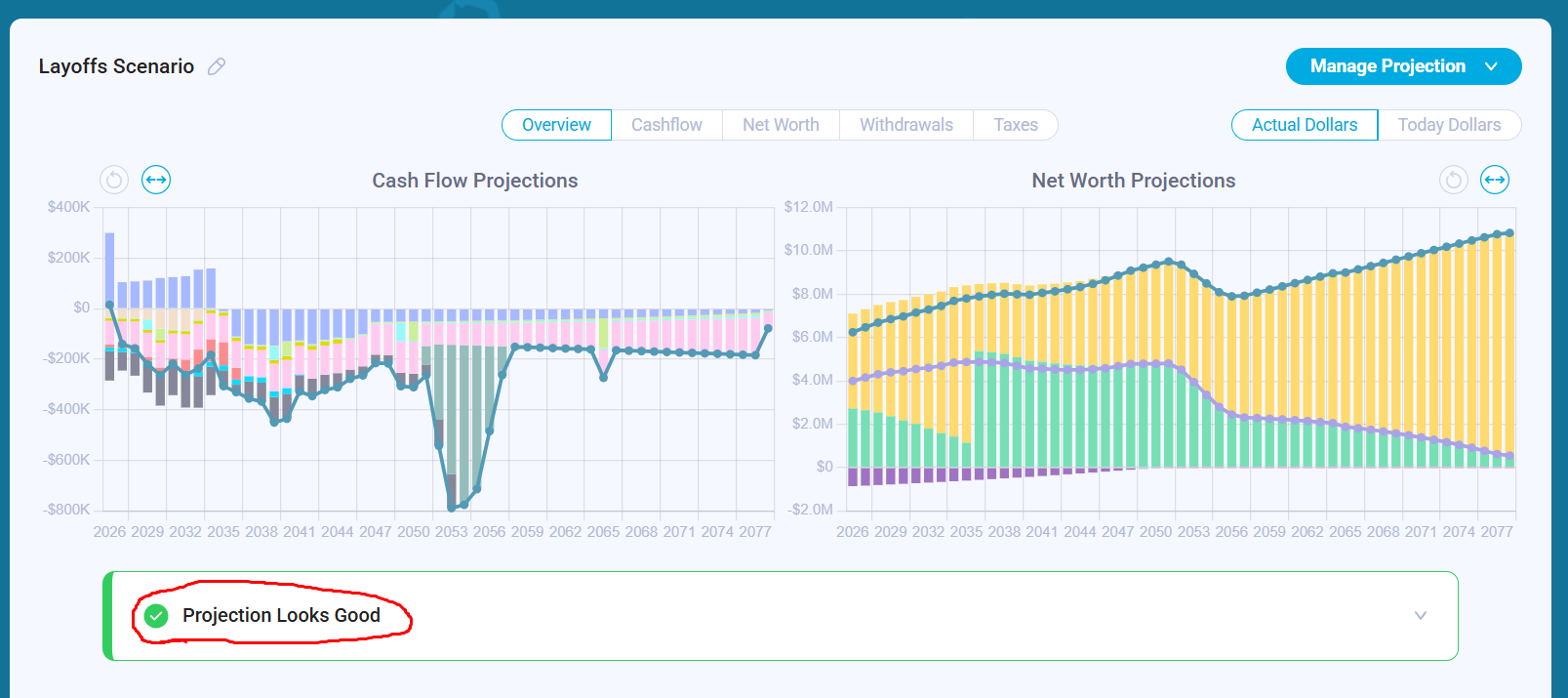

Finding a new job takes time, and it’s a good idea to be conservative when doing financial planning and assume that finding a new job may take not 3-6 months but 12-18 months. For that, the family go to their financial projection and make the following changes:

Set the current job to stop now

Estimate and add severance package

Start a similar job 12-18 months from now

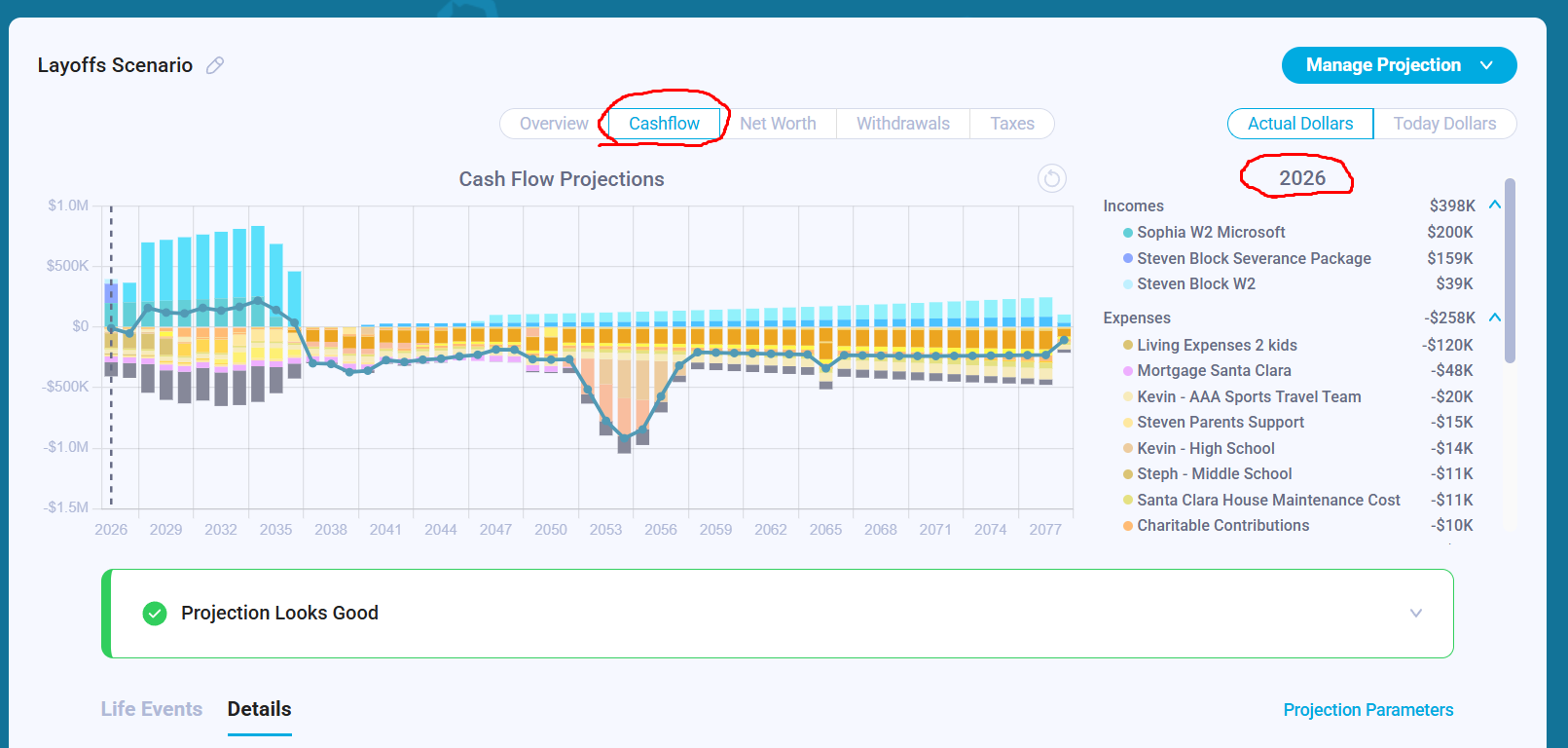

Companies normally share severance package details in advance. The family takes that information, estimates the severance payment and adds it as an ordinary W-2 income so the model could properly estimate their income taxes:

Before adding a new job, it’s a good idea to look if the projection still holds. Many people who spent decades in tech and worked at successful companies whose stock significantly appreciated are already financially independent, especially if they are willing to cut some of their discretionary expenses:

When the second job is added, the family can see their updated annual budget and reserve funds to cover the budget deficit. This specific family now has a small deficit in the next 2 years and they won’t be able to save:

2026 = $13K annual deficit (previously, $159K profit)

2027 = $35K annual deficit (previously, $178K profit)

Updating Financial Goals

Now, when the expected income is updated and future expenses are decided by the family, they want to recalculate their financial goals. From the projection, they already know that they won’t be able to save. That said, they still may contribute into their 401K and IRA accounts as the second partner still works and contributions to 401K reduce taxable income. That said, it’s going to be more of a transfer from taxable to tax-deferred and tax-free accounts rather than saving because the family is expected to spend more than they make in 2026/2027.

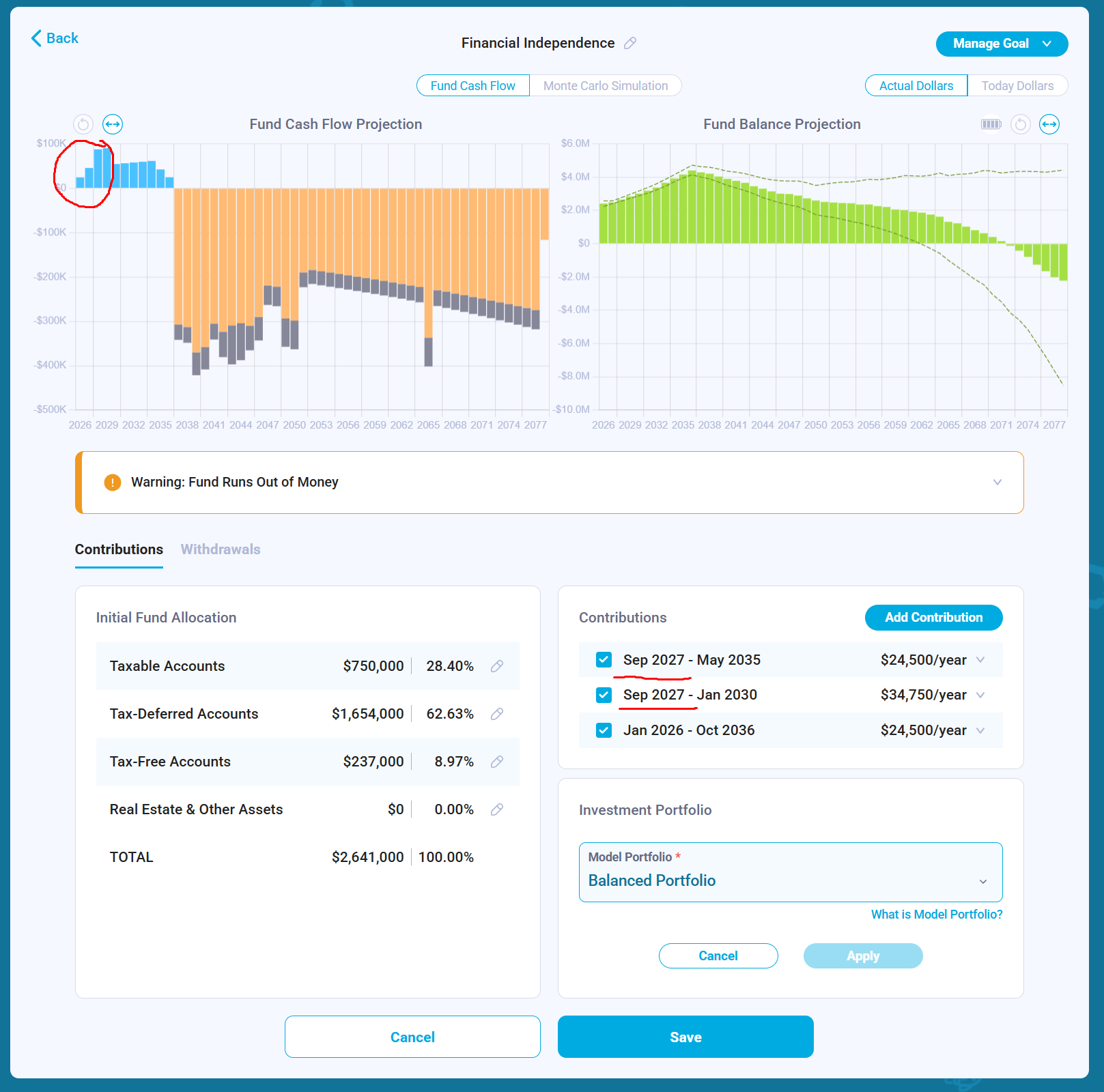

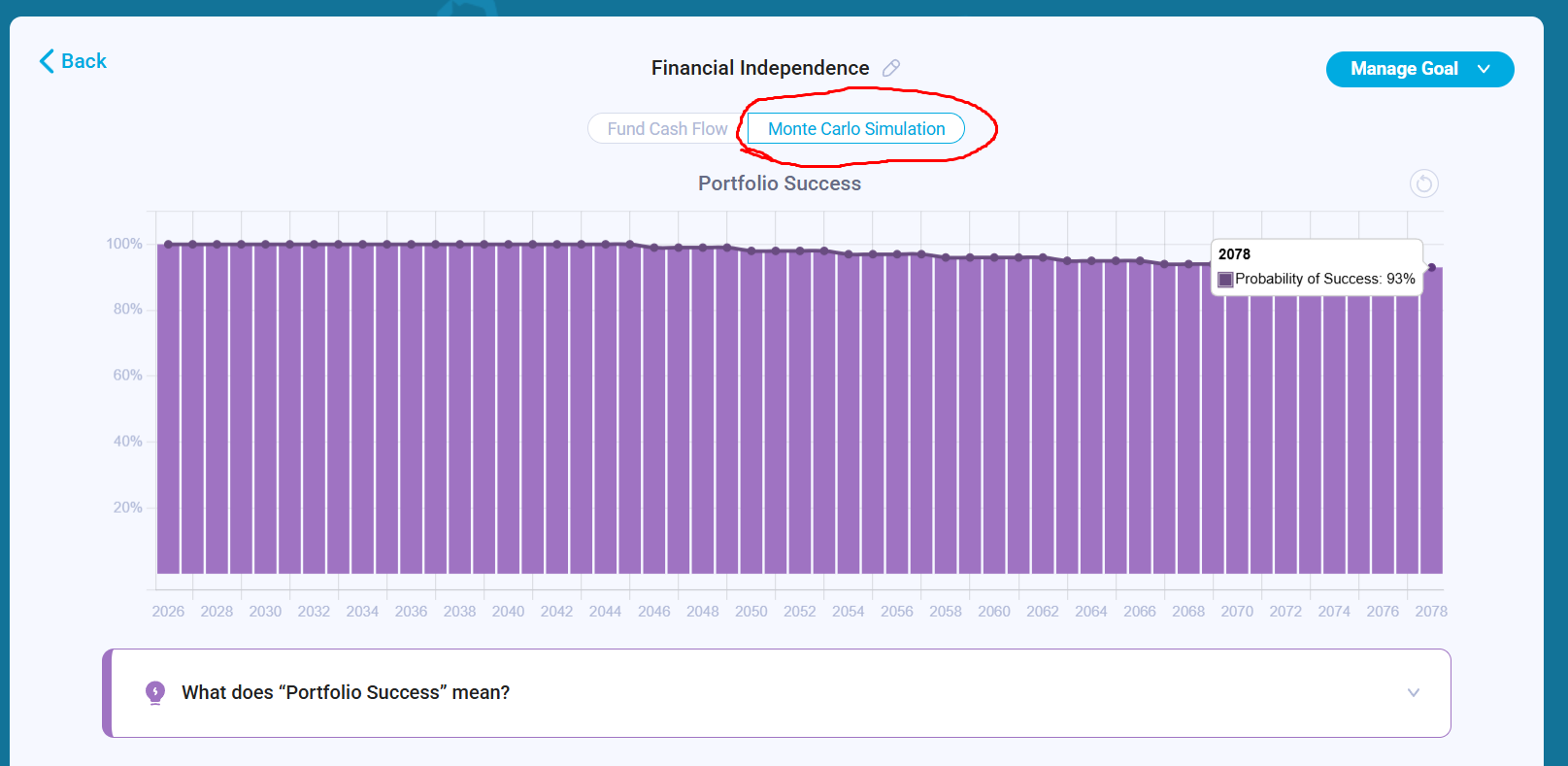

The family reduces their 401K contributions and plans to continue them starting September 2027. That makes the fund p5 percentile to run out of money in 2061. The family is targeting 95% success chance for their fund and fund duration is until partners turn 95 years old:

The family has three options now:

They either can increase their initial fund allocation

They can delay their retirement and withdrawals from the fund by 1-2 years

They can do nothing and accept lower chances (92%) of success instead of initially planned 95%.

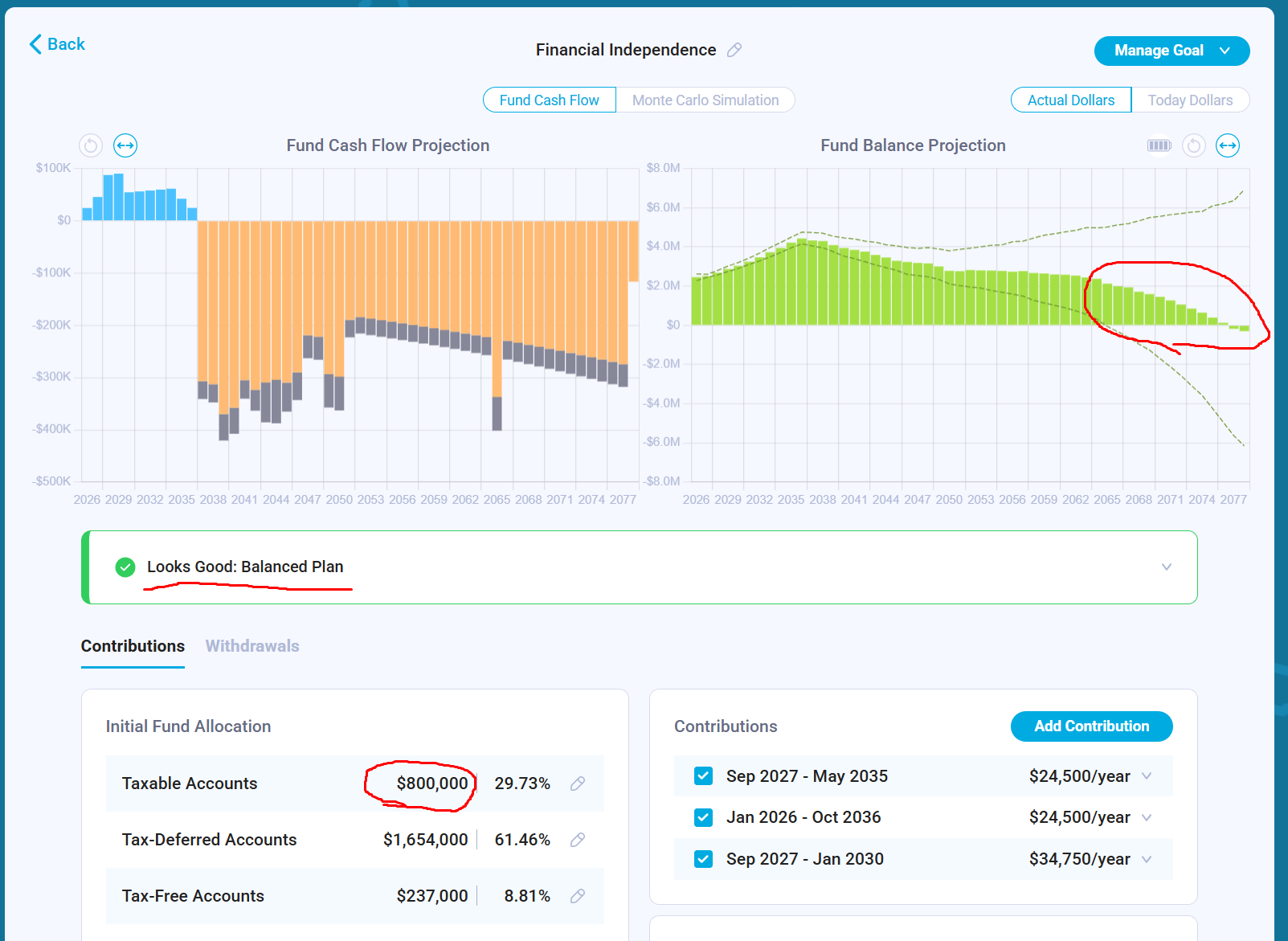

The family has $1M not allocated towards any financial goal at the moment, so they simply can increase their allocation from $750K in taxable accounts to $800K to make their plan balanced again:

Then they review their Success Chances in Monte Carlo Simulation and adjust allocations and contributions if they think their success chances are too high or too low. It’s natural to want to have a 100% success rate when setting financial goals. But the truth is that when it comes to investing, 100% chances is a signal that the investor is either over-saving for their financial goal or under-investing which most of the time leads to regrets in the future.

As investors, we would like to take a reasonable amount of risk. For each financial goal and person it’s going to be different.

Preparing Funds

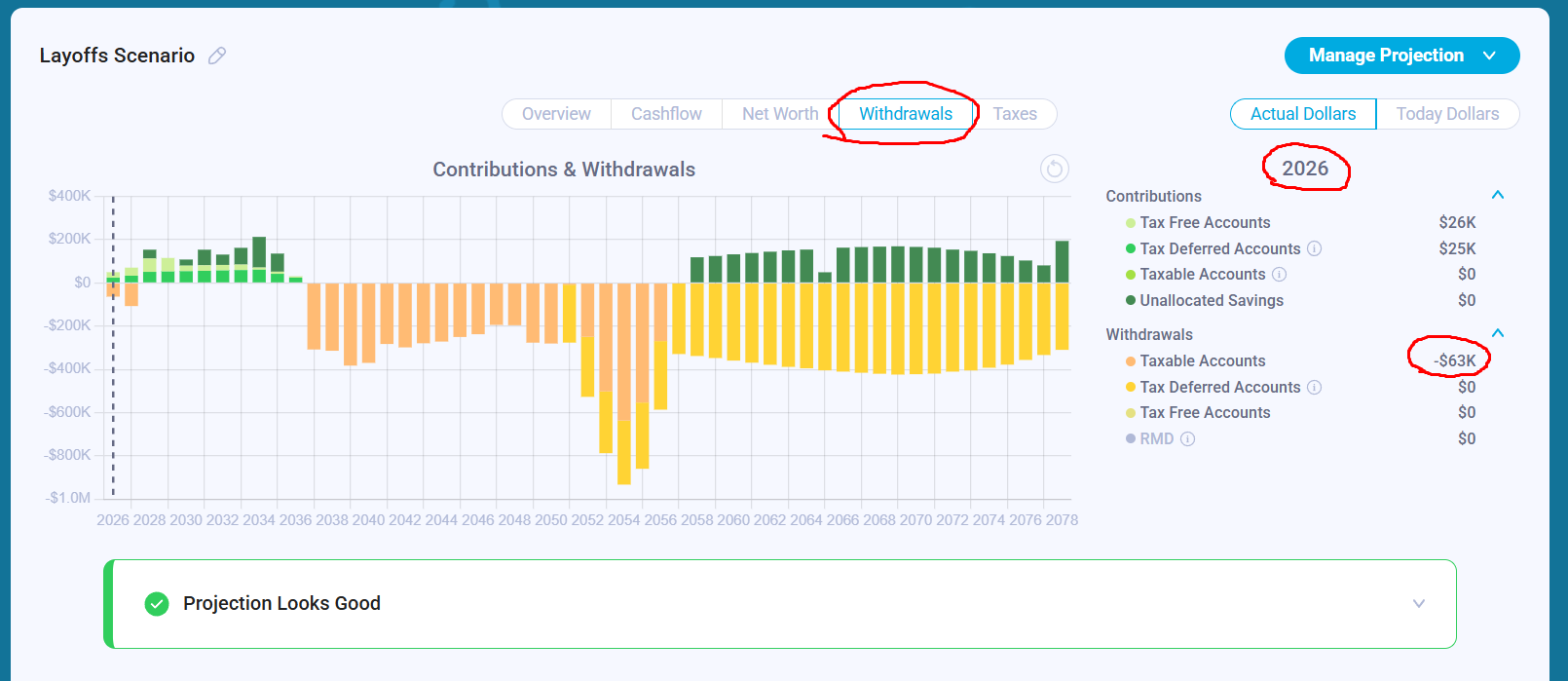

Now the family should prepare their funds and make sure their portfolio reflects that. For that they can go back to Financial Projection and review their “Withdrawals”. The family is expected to have a deficit of $13K in 2026 and $35K in 2027. But because they would like to continue contributing into their 401 and IRA accounts, they’ll need to withdraw $63K and $106K in 2026 and 2027 accordingly from their taxable accounts.

They know that they should keep these amounts in low-risk and liquid funds available for withdrawals:

Conclusion

A layoff is a significant life event, but it does not have to be a financial catastrophe. The difference between a stressful job hunt and a strategic career pivot lies in the clarity of the plan. As we have explored, a robust financial plan serves three critical functions:

Emotional Stability: It replaces the “scarcity mindset” with data, allowing you to reject unsuitable roles and wait for the right opportunity.

Agility: By modeling “what-if” scenarios (such as extended unemployment or reduced contributions), you can identify which levers to pull, whether that is cutting discretionary spending or reallocating taxable assets.

Intentionality: It forces a conversation about what truly matters. If a family discovers they are already near financial independence, a layoff might not be a setback at all—it might be the nudge needed to start a business or focus on long-delayed personal goals.

Ultimately, the best time to build a financial plan is when things are going well, but the best time to use it is when they aren’t.

P.S. If you want to explore these trade-offs using your own inputs, tools like Nauma are designed to help you build and stress-test different scenarios.

For those who want help going deeper, we also work with a small number of clients to build custom models tailored to their career, family, and risk profile. We currently have availability in April and May 2026. Details are here.