'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Strategically moving assets from tax-deferred accounts, such as traditional IRAs or 401(k)s, into tax-free Roth accounts may reduce future Required Minimum Distributions (RMDs), lower a family’s total lifetime tax bill, and reduce taxes when passing wealth to heirs.

But doing this manually is incredibly difficult. Roth conversions require setting aside funds in taxable accounts to pay the resulting taxes, especially if the conversions are done before age 59½. This creates additional pressure on taxable accounts and may lead to liquidity issues if the family stopped working early. A family may find itself in a situation where it technically has assets, but those assets are not available to cover current needs because they are held in illiquid retirement accounts, deferred compensation, real estate, or PE/VC funds.

For people over age 59½, the main challenge often comes from health insurance. They may need to keep MAGI, or Modified Adjusted Gross Income, below certain thresholds to qualify for ACA premium subsidies and avoid IRMAA surcharges when they switch to Medicare.

In both cases, it can be hard to tell whether Roth conversions actually increase family wealth because a direct comparison is often not straightforward: assets in tax-deferred accounts are not equivalent to assets in tax-free accounts.

If you do Roth conversions without a clear strategy, you are left in the dark about whether the strategy is actually optimal.

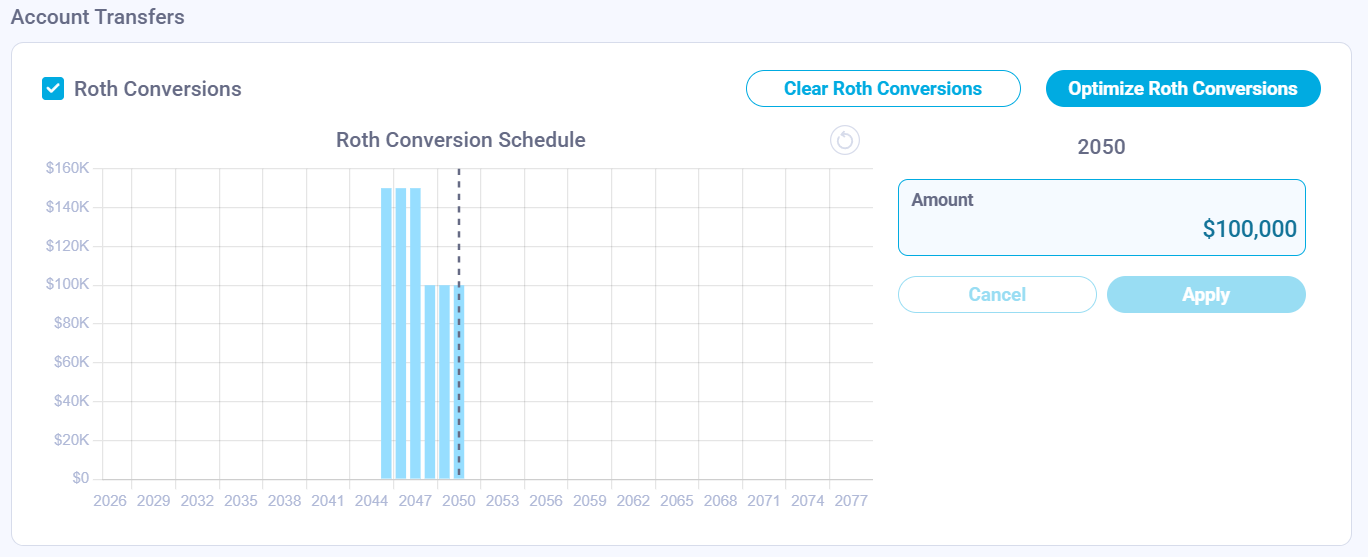

Roth Conversion Optimizer

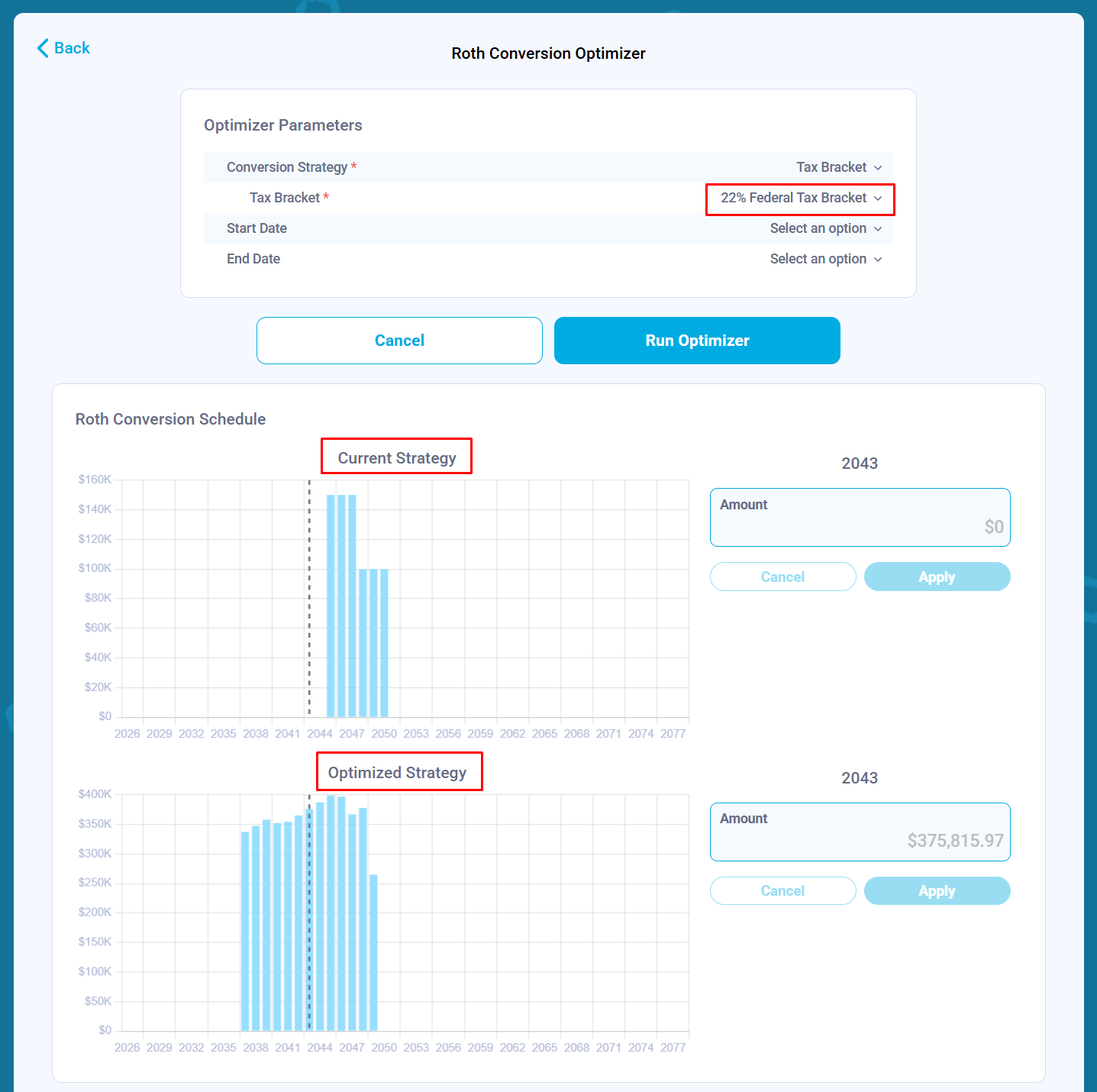

To solve this, we just built a new feature: the Roth Conversion Optimizer. We have added an “Optimize Roth Conversions” button directly inside your financial projection dashboard. When you click it, the system prompts you to choose an optimization strategy. Currently, the platform supports the Tax Brackets strategy.

When you select this strategy and input a target federal tax bracket (for example, 22%), our solver runs a binary search algorithm across the years between your specified start and end dates. It automatically calculates the exact amount needed to increase your taxable income and execute Roth conversions right up to the ceiling of that specific federal tax bracket.

However, as we rolled this tool out, it highlighted a financial planning lesson: blindly optimizing for federal tax brackets, one of the most common approaches in financial planning tools, and ignoring state and foreign taxes can backfire and cost millions of dollars.

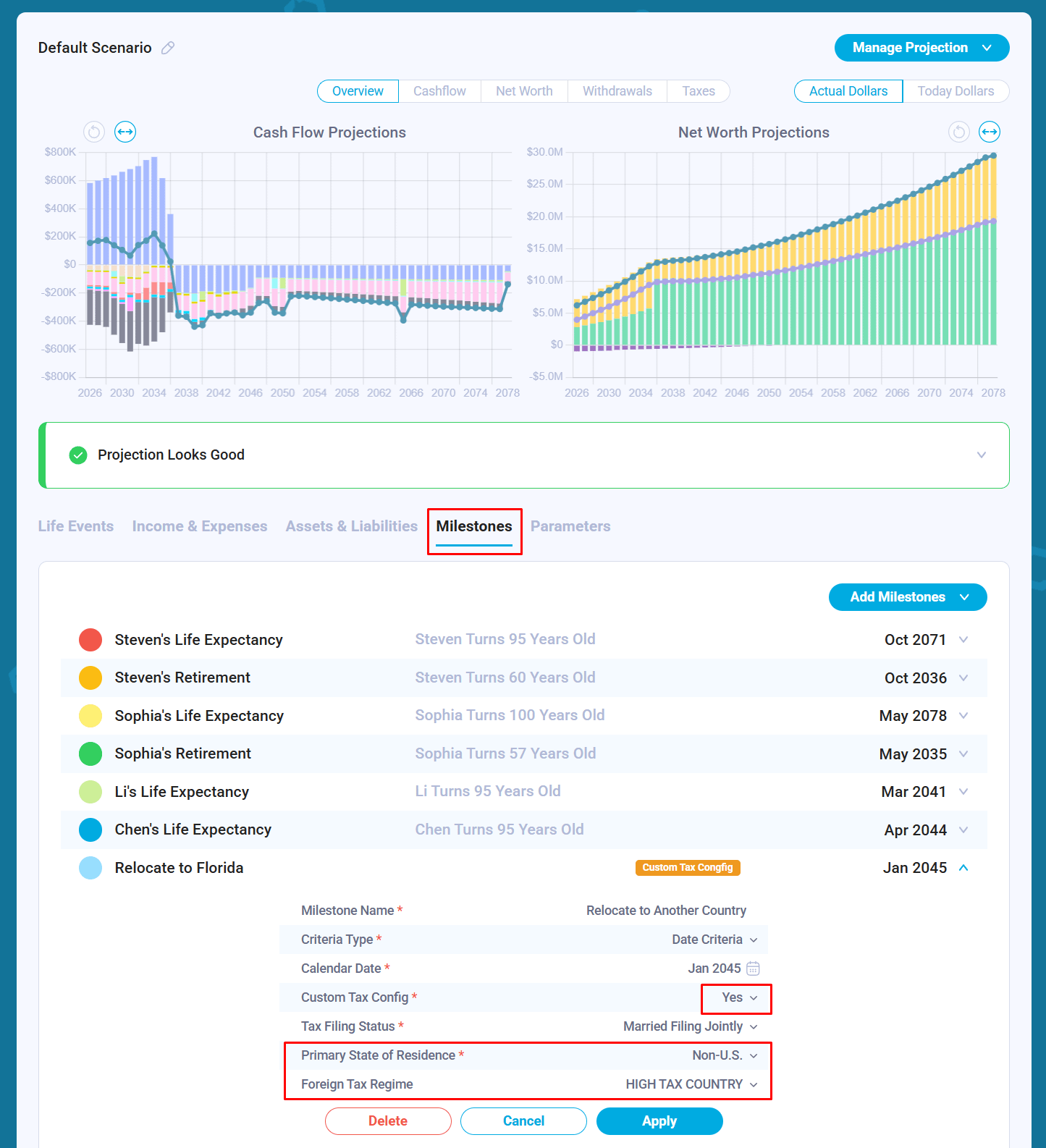

Problem #1: The Interstate Move (California to Florida)

To see why optimizing solely for a federal tax bracket can backfire, let’s look at a case study of a family currently living in California that plans to relocate to Florida in 2045. If we blindly run the optimizer to fill the 22% federal tax bracket across the entire projection, the results look highly counterintuitive:

Current Strategy: Manual Roth Conversions

Total lifetime tax paid: $4.6 million

Terminal net worth: $29.5 million

Optimized Strategy: Filling the 22% Federal Bracket

Total lifetime tax paid: $4.9 million

Terminal net worth: $25.1 million

Why did an “optimizer” make this family $4.4 million poorer?

Because the family lives in California before 2045, accelerating income through early Roth conversions subjects them to California’s high progressive state tax rates. During the conversion years, their state tax bill increases from a baseline of $14,000 to nearly $60,000. Since they plan to move to tax-free Florida later, accelerating income while still living in California destroys value. The direct tax cost is higher, and the assets used to pay those taxes no longer remain invested and compounding.

Problem #2: The Expat Double-Tax Friction (Retiring Abroad)

The problem becomes even more pronounced for families planning to leave the U.S. and retire abroad. Let’s look at another example. Instead of moving to Florida, the family decides to relocate to a country with a high-tax regime, such as a flat 20% income tax rate starting at the first dollar of income, with no standard deduction.

Because they are U.S. citizens, they remain subject to U.S. federal income tax on their global income, including Roth conversions. At the same time, they may also be subject to the local tax laws of the foreign country.

When we run the 22% federal bracket optimizer on this international track, the numbers look like this:

Current Strategy: Manual Roth Conversions

Total lifetime tax paid: $7.8 million

Optimized Strategy: Filling the 22% Federal Bracket

Total lifetime tax paid: $6.3 million

At first glance, you might think, “Great! The optimizer saved them $1.5 million in taxes.” But that conclusion would be premature. The solver is still blind to the international context. It is only looking at U.S. federal tax brackets and ignoring the 20% foreign tax overlay. It does not account for how the destination country treats Roth conversions, whether that country recognizes the tax-free status of Roth accounts, or how foreign tax credits apply.

Using a standard, single-dimensional federal bracket optimizer when relocating abroad is a roll of the dice. It may produce a good result, or it may create an unexpected global tax bill.

A federal tax bracket optimizer may work reasonably well for families who plan to retire in their current tax environment. Families considering interstate moves or retirement abroad should be much more careful.

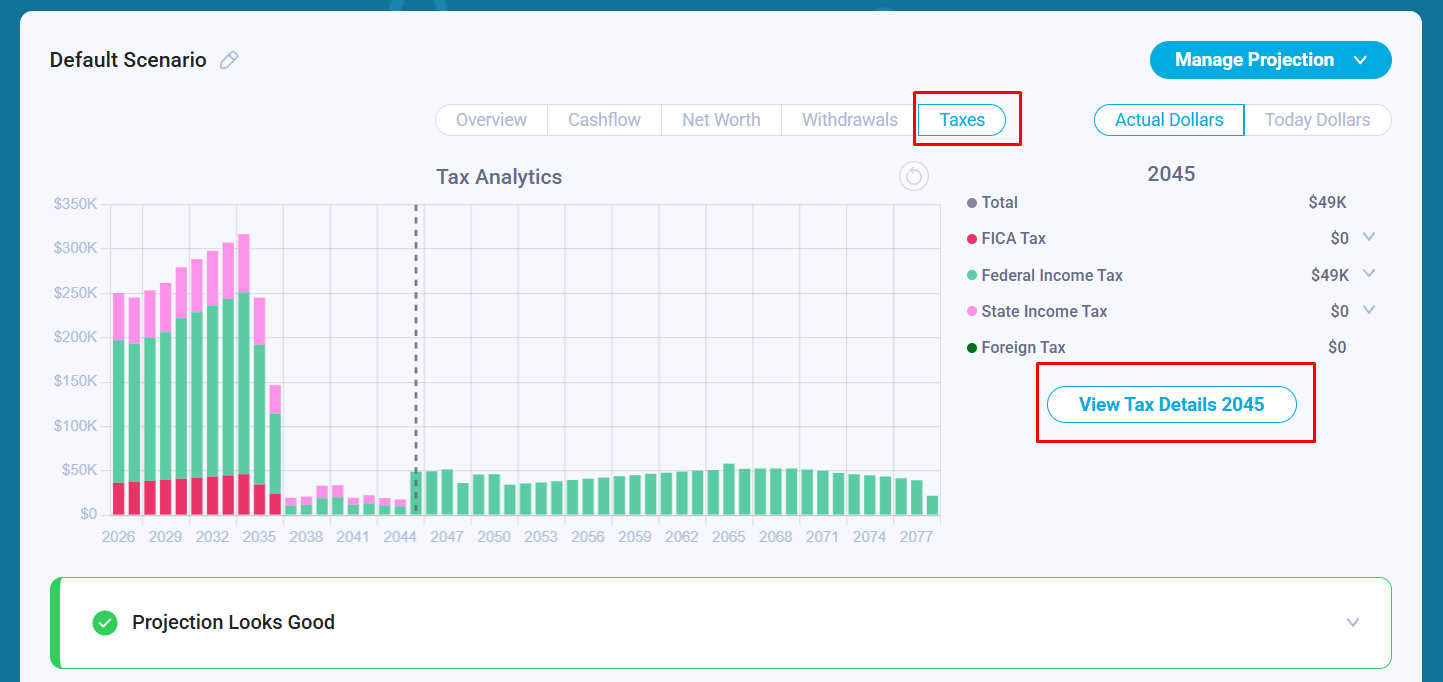

Verifying Roth Conversions

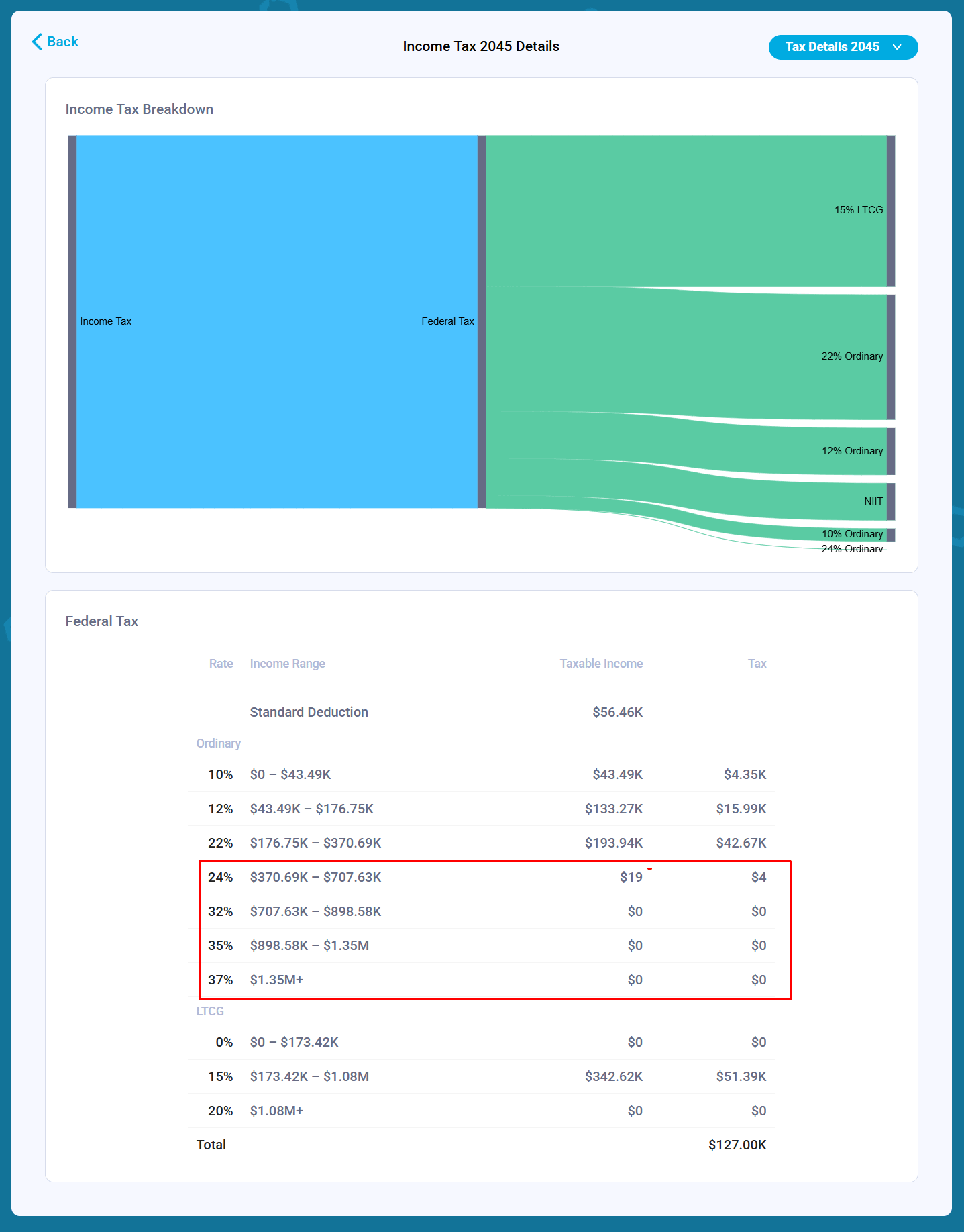

If you choose to apply an optimized strategy, you can audit the tool’s precision by clicking into any specific year on your timeline and reviewing the granular tax details. If you set the target bracket to 22%, you should generally see no taxable income above the 22% tax bracket in the year the optimizer adds a Roth conversion.

You may occasionally notice a tiny amount, such as $27 or $50, appearing in the next highest tax bracket. This is by design. To maintain high performance, our solver uses a binary search algorithm with a precision threshold of $100. The algorithm stops searching once it gets within $100 of the target, which means a small number of dollars may spill into the next bracket.

If you require absolute, single-dollar precision for your models, let us know and we can tighten the threshold.

What We Are Building Next: Terminal Wealth Optimization

This feature illustrates well why standard, single-dimensional federal tax bracket optimization is an incomplete tool for high-net-worth families with dynamic lives. True financial optimization cannot look at federal brackets in isolation.

To build a more robust optimization engine, we are developing a solver that optimizes against Terminal Wealth: maximizing the exact amount of money you have left at the end of your life expectancy. To do that, the next iteration of our optimizer will factor in the comprehensive, multi-jurisdictional tax picture simultaneously:

Federal Income Taxes

Progressive State Income Taxes

Foreign/Expat Tax Treaties and Local Rates

By calculating how these compounding layers interact with specific life events, such as moving states or retiring abroad, Nauma will be able to estimate the net impact of cross-border tax friction on a family’s portfolio and solve for a more efficient Roth conversion strategy.

About the Author: Alex Sukhanov, founder of Nauma, a financial planning platform built for people in tech and high-net-worth families. Alex previously worked at Google and started Nauma to help more people in tech make better financial decisions and achieve more in their lives. You can reach out to Alex on linkedin.

Nauma is supported entirely by its users with no commissions and no affiliate incentives. It is designed to give people clarity on taxes, equity compensation and retirement planning.

Disclaimer: Nauma projections are hypothetical and not guarantees of future results. Tax laws may change, and estimates may not reflect future legislative updates. This content is for educational purposes only and is not tax or investment advice.