'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Discretionary vs. Non-Discretionary Goals

Why Classifying Your Retirement Spending as Fixed or Flexible Is One of the Most Important Decisions in Your Financial Plan

A non-discretionary goal is one that is typically treated as non-negotiable regardless of market conditions, investment performance, or unexpected life events — spending that cannot be meaningfully reduced without affecting health, housing security, or basic quality of life. A discretionary goal is one that can be reduced, deferred, or eliminated if necessary.

This distinction may seem simple. In practice, it is one of the highest-leverage decisions in financial planning. Whether a spending category is fixed or flexible determines how your plan treats it under stress — how much probability of success it requires, how it interacts with sequence of returns risk, and what happens to your retirement plan if markets underperform in the years immediately after you stop working.

Non-Discretionary Goals: The Funded Floor

Non-discretionary goals represent the minimum a plan is typically designed to deliver. These are the spending categories that are difficult to reduce without materially degrading health or quality of life. They form the funded floor — the level of retirement income that financial planners commonly target with high confidence. A probability of success in the range of 80–95% in a Monte Carlo simulation is often used as a reference point for this floor, though the appropriate target depends on individual circumstances. Monte Carlo results represent statistical probabilities, not guarantees of future outcomes.

For most Nauma users in retirement, non-discretionary spending includes:

Housing. Mortgage or rent payments, property taxes, homeowners insurance, and basic maintenance. If your home is paid off at retirement, this category shrinks substantially — which is one concrete reason mortgage payoff before retirement improves retirement plan robustness.

Healthcare. Medicare Part B and Part D premiums, supplemental insurance (Medigap or Medicare Advantage), out-of-pocket medical costs, and long-term care costs if not funded through a separate insurance policy. For reference, the standard Medicare Part B monthly premium is $202.90 in 2026 (with an annual deductible of $283), though premiums vary by income level. Healthcare is one of the most inflation-sensitive categories in retirement — costs tend to grow faster than the general CPI.

Basic food and utilities. Groceries, electricity, gas, water, and internet service. These have limited flexibility — you cannot meaningfully cut essential nutrition or heat.

Transportation. A single vehicle's operating costs, insurance, and fuel for necessary travel. Medical appointments, grocery runs, and basic mobility are non-discretionary for most retirees.

Minimum lifestyle maintenance. Clothing, personal care, and household expenses consistent with a basic but comfortable standard of living. Not luxury — the minimum needed to maintain health and dignity.

These items share a common feature: they have no flexible substitute. You cannot defer a property tax bill. You cannot opt out of Medicare premiums. If markets perform poorly in years 2 and 3 of your retirement, these expenses still need to be paid — which is precisely why they need to be modeled separately and funded to a high probability.

Discretionary Goals: The Adjustable Upside

Discretionary goals improve quality of life but can be scaled back without catastrophic consequences. They can be reduced, deferred, or temporarily eliminated if a market downturn or unexpected event makes full funding difficult. The goal is not to eliminate them — it is to recognize that they can flex if necessary, and to plan accordingly.

For a typical Nauma user, discretionary retirement spending includes:

Travel. International trips, extended vacations, adventure experiences. Many retirees front-load travel in their early active years (ages 60–75), then taper naturally. Both the amount and the timing are flexible.

Dining and entertainment. Frequent restaurant meals, event tickets, club memberships, hobby spending. These can be scaled materially without changing the fundamentals of daily life.

Gifts and charitable giving above a committed baseline. Annual pledges to specific institutions may feel non-discretionary; spontaneous or aspirational giving is generally discretionary. The line is typically drawn based on personal values and the degree to which a commitment is firm versus aspirational.

Second homes and investment properties. The carrying costs of properties beyond your primary residence — taxes, insurance, maintenance, HOA fees. These can be eliminated if necessary by selling the property.

Legacy and inheritance goals. What you plan to leave behind. For purposes of retirement modeling, legacy goals are generally classified as discretionary, as no one's day-to-day retirement security depends on what is left to children or charity. That said, the personal importance of legacy varies widely and is ultimately a matter of individual values.

Why the Distinction Matters for Retirement Probability Modeling

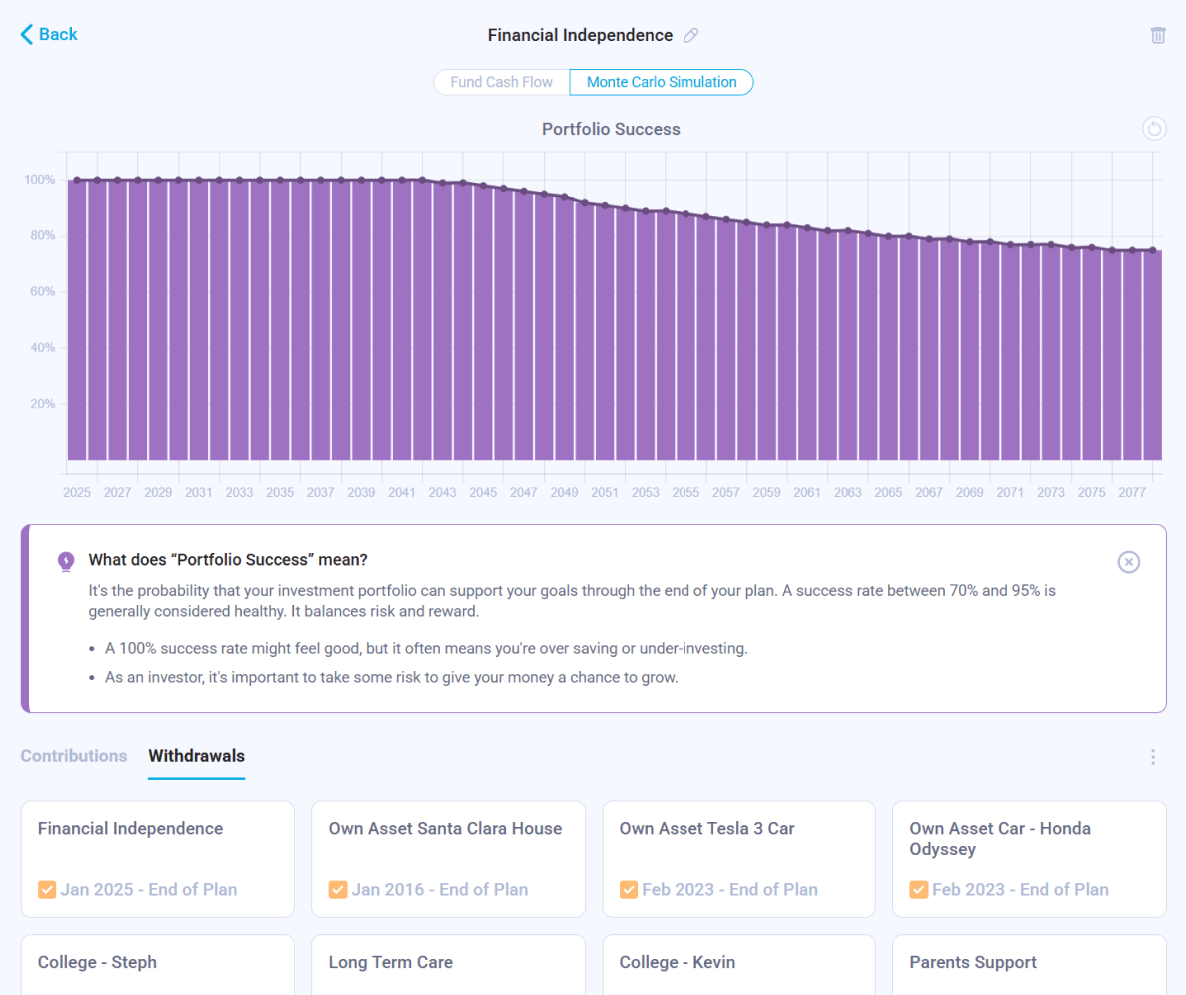

When Nauma or any financial planning tool runs a Monte Carlo simulation, it simulates thousands of possible future market scenarios and asks: in what percentage of those scenarios does your plan succeed — meaning you never run out of money?

The result depends critically on how you define success. If success means funding every dollar of planned spending (discretionary and non-discretionary alike) in every scenario, the bar is very high. If success means funding only non-discretionary spending in bad scenarios while discretionary spending flexes down, the plan has much more room to maneuver — and a higher probability of meeting the minimum standard.

Monte Carlo simulations are statistical tools that model a range of possible outcomes based on assumptions about returns and volatility. They represent probabilities, not predictions, and do not guarantee any specific outcome.

Consider a plan with $12,000 per month in total planned spending, of which $7,500 is non-discretionary and $4,500 is discretionary:

- Probability of funding the full $12,000/month: 71%

- Probability of funding the non-discretionary floor of $7,500/month: 95%

Both numbers are meaningful. The 71% tells you how likely you are to maintain your full preferred lifestyle. The 95% tells you how likely you are to remain housed, healthy, and comfortable. A plan that looks risky by one measure may be quite secure by the other.

This dual-probability framing — funded floor probability plus full-plan probability — is how Nauma structures retirement risk analysis. Knowing both numbers makes risk management decisions much clearer.

Discretionary Goals and Sequence of Returns Risk

Sequence of returns risk is the danger that poor investment returns in the early years of retirement permanently impair your portfolio, even if long-term average returns are acceptable. The reason: withdrawals during a down market lock in losses, reducing the capital available to recover when markets improve.

Discretionary spending flexibility is one of the most powerful tools for managing sequence of returns risk. If markets decline 35% in your first two years of retirement, a plan that allows you to cut discretionary spending from $4,500 to $1,500 per month during those years reduces withdrawals by $36,000 per year, preserves capital, and may significantly improve the plan's long-term trajectory. Spending flexibility reduces risk, but does not eliminate it — including the risk of loss of principal.

A plan with no discretionary flexibility — where all spending is treated as non-negotiable — cannot make this adjustment. It withdraws the same amount in a down market as in a good one, accelerating portfolio depletion at the worst possible moment.

This is why classifying your spending before retirement is not an academic exercise. It defines the range of responses available to you if things go wrong — and the plans that survive bad markets are often the ones with the most pre-planned flexibility.

See Sequence of Returns Risk for a full explanation of the mechanics and how spending flexibility mitigates the damage.

How to Classify Your Own Goals

The test for whether a goal is non-discretionary is straightforward: Would the failure to fund this spending meaningfully harm my health, housing security, or basic quality of life? If yes, it is non-discretionary. If no — if the spending improves life but its absence is tolerable — it is discretionary.

| Spending Category | Classification | Reason |

|---|---|---|

| Primary residence mortgage or rent | Non-discretionary | Housing security — cannot be eliminated |

| Medicare and supplemental insurance premiums | Non-discretionary | Health coverage — cannot be deferred |

| Groceries and utilities | Non-discretionary | Basic living costs |

| Long-term care insurance premium | Non-discretionary (typically) | Protects against catastrophic care costs |

| Annual international travel | Discretionary | Quality of life — can be reduced or deferred |

| Second home carrying costs | Discretionary | Optional asset — can be sold or rented |

| Dining out frequently | Largely discretionary | Comfort spending — significant flexibility exists |

| Charitable giving above committed baseline | Discretionary | Aspirational, not essential |

| Legacy and inheritance goal | Generally discretionary | Retirement security typically does not depend on it |

What Cutting Discretionary Spending Does to Monte Carlo Outcomes

The math is direct. A $4,000 per month reduction in discretionary spending equals $48,000 less per year in withdrawals. Over a 33-year retirement (age 62 to 95, a commonly used planning horizon), that is $1.58 million in reduced withdrawals — each dollar of which stays in the portfolio and continues compounding.

In a Monte Carlo simulation, the flexibility to cut $4,000 per month of discretionary spending in the bottom 20% of scenarios may improve overall plan success rates by 10 to 20 percentage points, depending on asset allocation, portfolio size, and the specific scenarios modeled. A plan that succeeds in 71% of scenarios without any flexibility may succeed in 85–90% of scenarios when discretionary flexibility is modeled in. These figures are illustrative; actual results will vary.

This is not just about being willing to cut spending in bad times. It is about having a pre-planned response to market stress that does not require a panicked last-minute decision.

This article is for educational purposes only and does not constitute legal, tax, or financial advice. All examples are hypothetical and for illustrative purposes only. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Spending flexibility reduces risk but does not eliminate it. Always consult a qualified financial planner before making decisions about your retirement spending plan.

Frequently Asked Questions

Model Your Spending Floor in Nauma

Tag each goal as discretionary or non-discretionary, and see how your plan probability changes — for the floor and for the full plan — across thousands of market scenarios.

Get Started for Free