'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

FIRE for Tech Workers

Financial Independence, Retire Early — The Complete Guide for Software Engineers and Tech Professionals

FIRE — Financial Independence, Retire Early — is the goal of accumulating enough wealth to cover your living expenses indefinitely, then choosing whether and how much to work. For most people this takes decades. For tech workers at well-compensated companies, the math can compress to 10–15 years. High base salaries, substantial equity grants, and access to tax-advantaged accounts create conditions that simply do not exist in most other fields. But the same complexity that accelerates the path also introduces traps that can delay or derail it.

What Financial Independence Actually Means

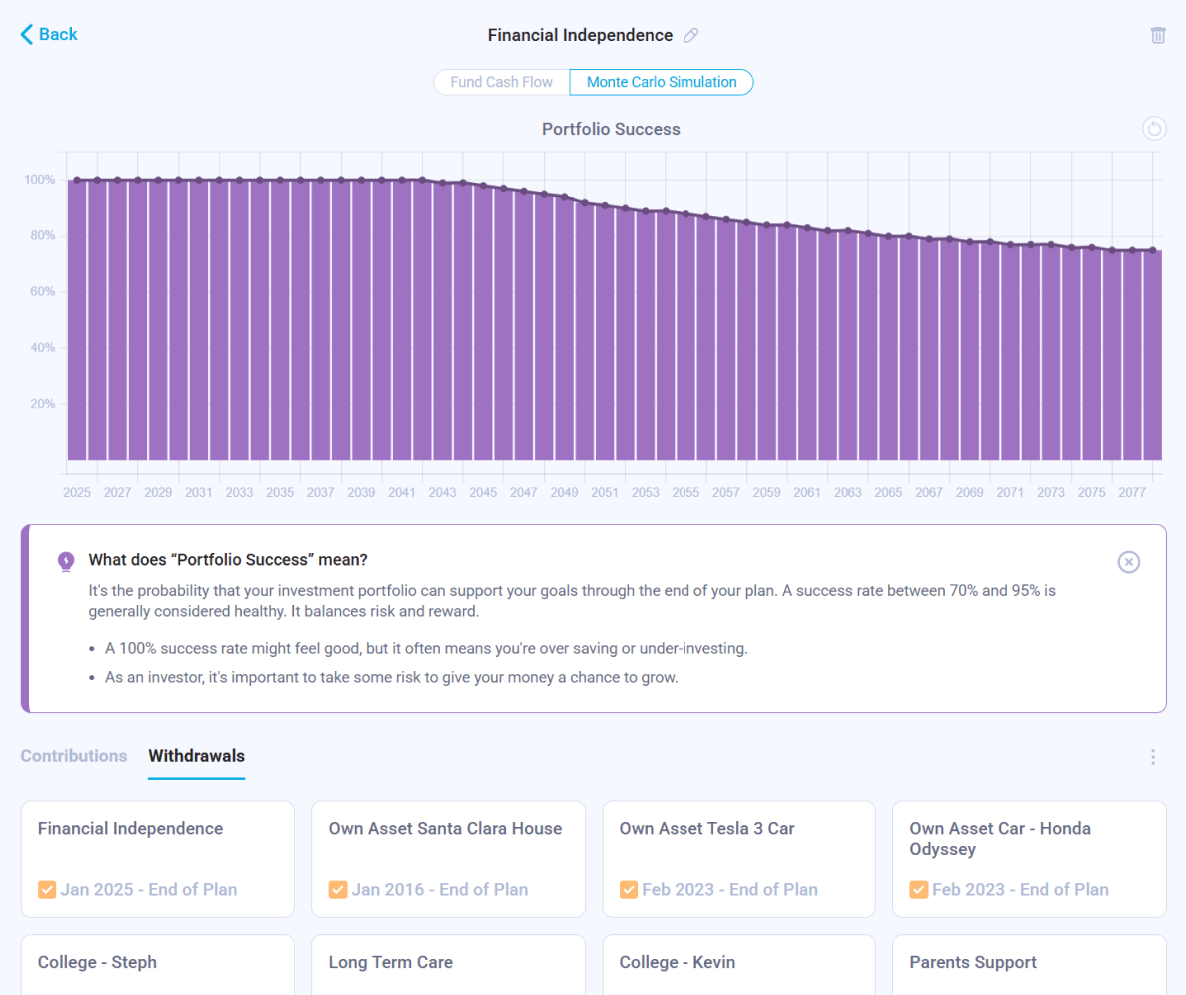

Financial independence does not mean you never work again. It means your investment portfolio generates enough income — or can sustain enough withdrawals — to cover your expenses without requiring earned income. The standard framework uses the 4% rule: divide your annual spending by 0.04 to find the portfolio size needed. Spending $120,000 per year requires a $3,000,000 portfolio. Spending $80,000 per year requires $2,000,000.

The 4% rule comes from the Trinity Study, which found that a portfolio of 50–75% stocks and 25–50% bonds survived 30-year retirement periods in 95%+ of historical scenarios when withdrawing 4% annually. For early retirees with 40- or 50-year horizons, many planners use 3–3.5% instead. The lower rate adds a meaningful buffer against long retirements and poor sequence-of-returns scenarios.

Why Tech Compensation Changes the Math

A typical senior software engineer at a large tech company in San Francisco or Seattle earns $250,000–$400,000 in total compensation — base salary, annual bonus, and vesting RSUs. A principal engineer or engineering manager at a top-tier company can exceed $500,000–$700,000. At these income levels, even moderate savings rates generate six-figure annual contributions to the portfolio.

The leverage is straightforward: someone earning $350,000 and spending $120,000 saves $230,000 per year before taxes. After maximizing tax-advantaged accounts and paying income tax, real annual savings might be $130,000–$160,000. At a 7% real return, $150,000 per year compounds to $3,000,000 in approximately 13 years. The same target takes 30 years at a $60,000 annual savings rate.

Equity compensation accelerates this further. A single RSU vest at a company whose stock has doubled since grant can equal two or three years of base salary savings in a single event. Many tech workers who reached FIRE did so primarily through equity, not salary accumulation.

The FIRE Number for Bay Area and Seattle Tech Workers

Geography matters enormously. A tech worker planning to remain in San Francisco post-retirement faces costs that are fundamentally different from someone planning to relocate. Bay Area spending for a couple with no mortgage — after paying off or leaving behind a home — might run $150,000–$200,000 per year including healthcare, property tax, travel, and normal living expenses. That implies a FIRE number of $3.75M–$5M at a 4% withdrawal rate, or $4.3M–$6.7M at 3%.

Many tech workers solve this by geo-arbitraging at retirement: leaving the Bay Area for a lower cost-of-living city or country and resetting their spending baseline. This is not a compromise — it is a deliberate leverage of the income earned in a high-cost market to fund a life in a lower-cost one. Moving from San Francisco to Austin, Lisbon, or Medellín can cut annual spending by 30–50%, which reduces the required portfolio by the same proportion.

Tax Strategy Is the Difference Between 12 Years and 16 Years

At high income levels, taxes are often the largest single expense. A tech worker earning $350,000 in California pays federal and state marginal rates that can reach 50%+ on the top dollar. Without deliberate tax strategy, a meaningful share of the savings potential evaporates. The core moves:

- Max every tax-advantaged account first. In 2025: $23,500 into a 401(k), $7,000 into an IRA (or backdoor Roth IRA if income exceeds limits), $4,300 into an HSA if on a high-deductible health plan. These reduce current taxable income and let the investment grow tax-deferred or tax-free.

- Use the mega backdoor Roth if your plan allows it. Some 401(k) plans permit after-tax contributions up to the IRS total limit ($70,000 in 2025, including employer match). If the plan also allows in-plan Roth conversions or in-service withdrawals, these after-tax contributions can be converted to Roth, sheltering an additional $40,000+ per year in tax-free growth. This is one of the most powerful tax tools available to high-income earners — and most people never use it.

- Manage RSU vesting and selling deliberately. RSUs are taxed as ordinary income when they vest, at your full marginal rate. You cannot avoid this. But you can control what you do with the shares after vesting. Holding RSUs beyond the vest date concentrates your risk in a single stock — usually the same company that employs you. The default correct action is to sell immediately upon vest and reinvest in a diversified portfolio. If you hold for more than one year from vest, any additional gain is taxed at long-term capital gains rates (0%, 15%, or 20%), but this benefit rarely outweighs the concentration risk at large employers.

- Harvest capital losses in taxable accounts. In years where positions in your brokerage account have declined, selling at a loss and immediately reinvesting in a similar (not substantially identical) fund locks in a tax loss that offsets capital gains or up to $3,000 of ordinary income per year. Unused losses carry forward indefinitely. This practice — tax-loss harvesting — is most valuable for high earners with large taxable accounts built from RSU proceeds.

- Plan Roth conversions in low-income years. The early retirement period before age 59½ — and especially before Social Security and RMDs begin — is often the lowest-income stretch of a FIRE retiree's life. If most of your wealth is in traditional 401(k) or IRA accounts, these years are an opportunity to convert to Roth at a lower marginal rate, reducing future RMD-driven tax spikes and creating a tax-free withdrawal pool for the back half of retirement.

The FIRE Ladder: Accessing Money Before 59½

One of the most common misconceptions about FIRE is that retiring before 59½ means paying a 10% penalty on retirement account withdrawals. This is avoidable with proper planning. Several strategies allow penalty-free access to tax-advantaged money before the standard retirement age:

- Roth contribution ladder. Contributions (not earnings) to a Roth IRA can be withdrawn at any time, at any age, without tax or penalty. If you have been contributing to a Roth IRA for years, those contribution dollars are accessible immediately. Roth conversions become available penalty-free after 5 years from the conversion date, so converting traditional IRA funds in the years before you need them creates a ladder of accessible money.

- Rule 72(t) / SEPP. Substantially Equal Periodic Payments allow withdrawals from a traditional IRA before 59½ without the 10% penalty, as long as you take fixed payments calculated by IRS-approved methods for a minimum of 5 years or until you reach 59½, whichever is longer. The payments are still taxed as ordinary income, but the penalty is waived.

- Taxable brokerage accounts. Money in a regular brokerage account has no age restrictions. Withdrawals are taxed as capital gains (long-term if held more than one year), not ordinary income — and at income levels below ~$94,000 for married filing jointly in 2025, the long-term capital gains rate is 0%. Many early retirees live entirely on taxable account withdrawals for the first decade of retirement while the tax-advantaged accounts continue to compound.

Healthcare: The Largest Overlooked Expense

Employer-sponsored health insurance is a benefit that disappears the moment you leave tech. A family plan that cost $500/month through your employer can cost $2,000–$3,000/month on the ACA marketplace at full price. For early retirees, healthcare is often the largest fixed expense in the budget — and the most volatile, given that premiums and deductibles change annually.

The ACA provides subsidies on a sliding scale based on income. In 2025, households earning below 400% of the Federal Poverty Level qualify for premium tax credits. For a married couple with no dependents, that threshold is approximately $83,000. Many tech FIRE retirees deliberately structure their withdrawal strategy to keep Modified Adjusted Gross Income (MAGI) below subsidy thresholds — drawing from Roth accounts and long-held taxable positions taxed at 0% capital gains rates, rather than from traditional IRAs that would generate ordinary income. This income management can save $10,000–$20,000 per year in healthcare premiums.

Equity at Departure: What Happens to Unvested RSUs and Options

Leaving a tech company forfeits all unvested RSUs and options — with no exceptions. For someone mid-vesting-cycle this can mean walking away from hundreds of thousands or millions of dollars of unvested compensation. The decision to leave requires weighing the opportunity cost of unvested equity against the value of time and independence.

The calculus depends on your vesting schedule. If you are 30 months into a 4-year RSU grant and the remaining 18 months will vest $300,000, those shares represent real money that your portfolio must generate to replace. At a 4% withdrawal rate, that $300,000 is equivalent to $12,000 per year of sustainable spending — or roughly 2–3 months of many Bay Area budgets. Only you can decide if the freedom is worth the cost.

For those holding stock options, the post-termination exercise window — typically 90 days — creates an additional decision point. Options that are in-the-money at departure must be exercised within that window or expire. For deep-in-the-money options at a pre-IPO company, the exercise cost plus tax can be significant. Know your position before you give notice.

The Sequence of Returns Problem in Early Retirement

Retiring into a market downturn is the primary financial risk for FIRE retirees. If your portfolio drops 30% in year one and you continue withdrawing, you sell shares at low prices that never recover to their full compounding potential. The same average return over 30 years produces dramatically different outcomes depending on when the bad years occur.

Tech workers who retired in late 2021 and experienced the 2022 drawdown — when growth stocks fell 50–70% and the broader market fell 20% — saw this risk materialize in real time. The standard mitigations are: maintain 1–2 years of expenses in cash or short-term bonds to avoid selling equities in a downturn, keep a flexible withdrawal strategy that reduces spending modestly in bad years, and avoid over-concentration in tech stocks (which tend to fall faster in risk-off environments than broad indices).

Fat FIRE vs. Lean FIRE: Choosing Your Target

The FIRE community distinguishes between Lean FIRE (retiring on a minimal budget, often $40,000–$60,000/year for an individual) and Fat FIRE (retiring on a generous budget, often $150,000+/year). Most tech workers, given their earning power and California-or-Seattle lifestyle, are aiming for Fat FIRE — and that is the realistic baseline for anyone planning to stay in a high-cost area or maintain travel and discretionary spending.

There is also Barista FIRE or Coast FIRE — variants where you stop aggressively saving but continue working in a lower-stress role whose income covers current expenses while the existing portfolio compounds untouched. For tech workers burned out on high-intensity engineering roles, this middle path — consulting, part-time work, or a less demanding employer — is often the realistic first step rather than a complete exit from work.

Frequently Asked Questions

Model Your Path to Financial Independence

Nauma builds your personalized FIRE projection — RSUs, tax strategy, account sequencing, and retirement income — so you can see exactly when you can stop working.

Get Started for Free