'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

What Is Dynamic Withdrawal?

How Adjusting Retirement Spending Based on Portfolio Performance Can Support a Higher Starting Withdrawal Rate — and Why Even Small Flexibility Makes a Meaningful Difference

A dynamic withdrawal strategy is an approach to retirement spending in which the annual withdrawal amount is adjusted based on portfolio performance rather than taken as a fixed, inflation-adjusted sum each year. Instead of withdrawing the same real dollar amount regardless of market conditions — the assumption underlying the classic 4% rule — a dynamic approach increases spending when the portfolio is performing well and reduces it modestly when the portfolio is under stress.

The core insight is straightforward: a retiree who is willing to spend slightly less in a bad market year significantly reduces the risk of permanently depleting their portfolio, because they are not forcing the sale of assets at depressed prices to meet a non-negotiable withdrawal. Even modest flexibility — a 10–15% spending reduction in a single bad year — has historically been shown in research models to have a disproportionate positive effect on long-term portfolio sustainability.

Why Fixed Withdrawals Create a Structural Problem

The failure mode of a fixed withdrawal strategy is specific and well-documented. When a retiree begins withdrawing at a fixed rate and markets decline early in retirement, two things happen simultaneously: the portfolio value falls, and the fixed withdrawal continues at the same nominal amount. This means the withdrawal, as a percentage of the now-smaller portfolio, has increased — sometimes significantly.

A portfolio that has declined 25% now requires the same annual withdrawal to come from a 25% smaller asset base. The withdrawal rate has effectively risen from, say, 4% to 5.3%. If markets recover, the portfolio may survive. If they do not recover quickly, the higher effective withdrawal rate accelerates depletion. This is the mechanism behind sequence of return risk: early bad returns paired with fixed withdrawals can permanently impair a portfolio even if long-run average returns are adequate. See What Is Sequence of Return Risk? for a full explanation of this dynamic.

Dynamic withdrawal breaks this feedback loop by reducing the withdrawal when the portfolio is stressed — lowering the effective withdrawal rate and giving the portfolio more time to recover.

The Guyton-Klinger Decision Rules

The most researched framework for dynamic withdrawal is the Guyton-Klinger system, published by financial planners Jonathan Guyton and William Klinger in 2006. It consists of three decision rules that govern when and how to adjust annual spending.

The Portfolio Management Rule suspends the annual inflation adjustment when the portfolio's investment returns in a given year are negative. In a standard fixed withdrawal strategy, withdrawals increase by inflation each year regardless of portfolio performance. Under this rule, if the portfolio declined last year, the withdrawal stays flat in nominal terms (no inflation adjustment that year). This is a modest constraint — it simply means spending does not increase, not that it decreases.

The Prosperity Rule increases spending by 10% when the current withdrawal rate has fallen to 80% or less of the initial withdrawal rate. This typically happens after a period of strong portfolio growth. If the portfolio has grown enough that the withdrawal now represents only 3.2% of the total (when the initial rate was 4%), the Prosperity Rule allows a 10% spending increase to capture some of the gains. This prevents the strategy from being perpetually austere during good times.

The Capital Preservation Rule reduces spending by 10% when the current withdrawal rate has risen to 120% or more of the initial withdrawal rate. If the portfolio has declined enough that the withdrawal now represents 4.8% of the total (when the initial rate was 4%), spending is cut by 10% for that year. This is the protective mechanism — it triggers a spending reduction before the portfolio reaches a critical level, rather than after.

The practical effect of these three rules is that spending varies within a range: it never falls more than 10% below its initial level in any single year (Capital Preservation Rule), and it increases when portfolio growth allows (Prosperity Rule). Research by Guyton and Klinger showed that following these rules historically allowed starting withdrawal rates of 5.2–5.6% with a 40-year planning horizon at the same probability of success as a fixed 4% rule — a meaningful increase in sustainable starting income. However, given current equity valuations and the interest rate environment as of 2026, researchers increasingly suggest treating these upper bounds with caution; a more conservative starting point within the dynamic framework may be prudent.

Note: These projections are based on historical back-testing and do not guarantee future results. Actual outcomes will depend on future market conditions, individual circumstances, and consistent adherence to the decision rules. This analysis does not account for taxes, advisory fees, or account-type-specific withdrawal constraints, all of which can meaningfully reduce effective income.

The Guardrails Approach

A simpler and increasingly popular variant of dynamic withdrawal is the guardrails approach, developed and refined by financial planner and researcher Michael Kitces and subsequently formalized by Morningstar researchers David Blanchett and Jonathan Guyton. Rather than defining three separate decision rules, the guardrails approach sets an upper and lower withdrawal rate boundary:

- Upper guardrail: If the current withdrawal rate rises above a defined ceiling (commonly 6% of the current portfolio value), spending is reduced — typically by 10%.

- Lower guardrail: If the current withdrawal rate falls below a defined floor (commonly 4% of the current portfolio value), spending is increased — typically by 10%.

The guardrails function as a portfolio dashboard: the investor monitors their current withdrawal rate relative to the portfolio, and adjusts spending only when the rate moves outside the defined range. Most years, no adjustment is needed.

Ongoing research on the guardrails approach has found that it may support a starting withdrawal rate approximately 10–20% higher than a fixed strategy with the same probability of success — primarily because the occasional spending reductions in bad years help prevent the portfolio from entering a rapid depletion spiral. That said, actual outcomes depend on the sequence of returns experienced and should not be treated as a guarantee.

How Much Flexibility Is Required?

A common concern about dynamic withdrawal is that spending reductions may be too large or too frequent to be practical. The research suggests otherwise. Studies on dynamic withdrawal consistently find that the required adjustments are relatively modest when the rules are applied early and consistently:

In historical simulations, the Capital Preservation Rule (Guyton-Klinger) or the upper guardrail trigger fires infrequently — typically fewer than five times over a 30-year retirement in most historical scenarios. The average spending cut when it does fire is 10% per event, not a permanent reduction. The spending reduction in one bad year often leads to a Prosperity Rule trigger a few years later, partially recovering the cut.

The practical implication for many retirees: if your retirement budget includes meaningful discretionary spending — travel, dining, entertainment, gifts — you may already have built-in flexibility that functions as an informal dynamic withdrawal system. Cutting a planned international trip in a year when the portfolio has declined 20% is a natural and manageable adjustment that has a surprisingly large effect on long-term portfolio sustainability.

Dynamic Withdrawal and Goal-Based Planning

Dynamic withdrawal is most useful when retirement spending is understood in two layers: a non-negotiable floor (housing, food, healthcare, utilities) and a discretionary layer (everything else). The dynamic rules — whether Guyton-Klinger or guardrails — apply to total spending, but in practice the cuts tend to come from the discretionary layer first.

This distinction matters for how the strategy is planned. A retiree whose essential expenses are covered by Social Security and a small pension — and whose portfolio withdrawal funds primarily discretionary spending — has enormous practical flexibility. The Capital Preservation Rule's 10% cut in a bad year is absorbed by reducing discretionary spending, not by cutting essential expenses. This is the situation where dynamic withdrawal works most naturally and most comfortably.

A retiree whose portfolio withdrawal funds a significant portion of essential expenses has less flexibility. In that case, a floor-and-upside framework may be more appropriate: guaranteeing the floor through non-portfolio income sources (Social Security, annuities) and applying dynamic withdrawal only to the upside portfolio. See What Is the Floor-and-Upside Strategy? for how this separation works in practice.

Dynamic Withdrawal vs. the Fixed 4% Rule

The comparison between dynamic withdrawal and the fixed 4% rule is not simply about which produces better returns — it is about which better matches how people actually spend in retirement and which provides more sustainable income.

The fixed 4% rule's primary advantage is simplicity: the annual withdrawal is calculated once and adjusted for inflation each year, regardless of market conditions. Its limitation is rigidity: it ignores information about the portfolio's actual condition, which means it may be overly cautious in good years (leaving significant wealth unspent) and dangerously optimistic in bad years (forcing continued high withdrawals from a stressed portfolio).

Dynamic withdrawal sacrifices some simplicity for meaningfully better portfolio outcomes and, for many retirees, better matches their actual spending behavior. Most retirees do not spend in a rigid, inflation-adjusted pattern — they spend more when they feel financially secure and less when they feel uncertain. Dynamic withdrawal formalizes this natural behavior into a consistent, rule-based framework.

For more on the foundational withdrawal rate concept that dynamic strategies improve upon, see What Is a Sustainable Withdrawal Rate?.

This article is for educational purposes only and does not constitute investment, tax, or financial advice. The strategies and projections described are hypothetical and based on historical market data; they do not account for trading costs, advisory fees, bid-ask spreads, or individual tax obligations — all of which can meaningfully affect real-world outcomes. Tax treatment of withdrawals varies significantly depending on account type (traditional IRA, Roth IRA, taxable accounts) and individual circumstances. Withdrawal strategies involve risk, and portfolio outcomes are uncertain. Historical research on withdrawal rates is based on past market conditions and does not guarantee future results. Individual circumstances, including spending needs, risk tolerance, and portfolio composition, significantly affect which approach may be appropriate. Always consult a qualified financial advisor before making retirement income decisions.

Frequently Asked Questions

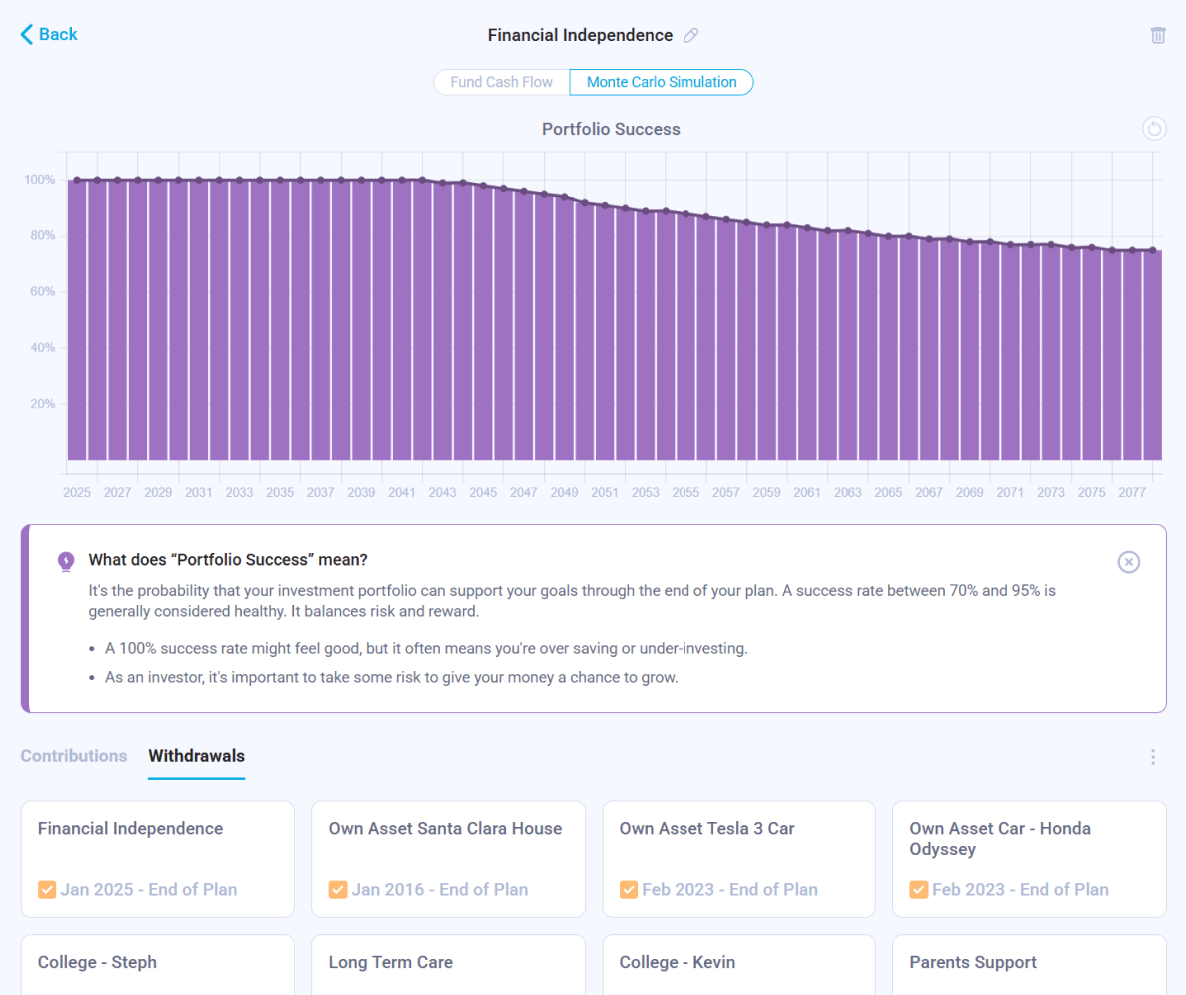

Model Your Withdrawal Strategy Across Market Scenarios

Nauma's Monte Carlo simulation shows how your retirement plan performs across hundreds of market scenarios — including how dynamic withdrawal rules change your probability of success.

Get Started for Free