'%3e%3cpath%20d='M136%2043.0521C135.893%2043.4991%20131.298%2041.3697%20123.51%2041.5186C120.787%2041.5712%20109.626%2040.8001%20104.06%2049.4228C101.316%2053.664%20102.266%2056.2491%20100.601%2061.5769C95.2065%2078.8661%2087.7394%2075.1856%2062.5302%2088.5228C54.5058%2092.764%2045.1595%20101.562%2043.5589%20103.087C31.9403%20114.163%2025.1664%20123.189%2025.1521%20123.171C25.1378%20123.162%2034.1912%20104.357%2047.7676%2082.7655C60.6795%2062.2429%2063.8235%2070.0769%2079.7722%2049.1336C81.7015%2046.6011%2084.8526%2037.6805%2089.683%2036.1032C93.6345%2034.815%2098.6148%2036.6114%20100.065%2038.5568C101.044%2039.8712%20101.459%2040.765%20103.831%2040.4408C110.048%2039.5996%20113.613%2039.8625%20115.492%2039.7748C116.95%2039.7047%20119.751%2039.915%20120.509%2039.9939C130.419%2040.9753%20136.15%2042.4563%20136.007%2043.0434L136%2043.0521Z'%20fill='%23127398'/%3e%3cpath%20d='M22.1867%2043.6392C30.3968%2055.0923%2031.5544%2062.348%2040.6506%2068.6923C45.9954%2072.4253%2053.4839%2075.4134%2058.2928%2075.5361C61.9084%2075.6325%2063.7305%2075.2557%2064.6023%2074.949C64.8524%2074.8614%2065.1025%2074.8351%2065.3597%2074.8263L76.0636%2070.6727C76.8068%2066.8871%2076.1637%2063.4784%2076.1065%2063.1892C75.0561%2058.0103%2072.3337%2053.3835%2070.5402%2051.2542C55.4561%2033.3428%2055.8062%2034.298%2046.5814%2028.0237C26.7884%2014.5902%20-1.22192%2021.3464%200.0428309%2022.0562C0.55016%2022.3454%2010.2394%2026.9634%2022.1867%2043.6392Z'%20fill='%23127398'/%3e%3cpath%20d='M79.8366%2044.0161C81.33%2046.4784%2083.4093%2051.5784%2083.7666%2056.8975C83.7952%2057.3094%2084.1667%2064.0393%2080.4654%2068.4733C78.5004%2070.8217%2076.2281%2071.5403%2075.585%2071.7506C61.487%2076.5264%2028.4319%20116.196%2023.3515%20133.494C23.2229%20133.941%2022.6227%20136.026%2022.5655%20136C22.3797%20135.921%2023.5373%20120.753%2028.925%20106.303C28.925%20106.303%2033.7196%2090.5295%2046.7387%2073.9326C49.1896%2070.8042%2052.8052%2067.0362%2052.8052%2067.0362C54.2414%2065.1434%2059.8006%2068.3068%2066.1887%2068.482C69.9401%2068.5872%2073.2198%2067.6846%2073.2055%2067.3604C73.2055%2067.2377%2073.0698%2067.0712%2072.8911%2066.9047C72.3195%2066.3702%2071.5907%2066.1423%2070.8761%2066.2475C69.9758%2066.379%2068.1323%2066.3877%2064.5738%2065.5903C59.8435%2064.5212%2052.8481%2060.096%2048.0534%2055.364C39.9076%2047.3109%2039.7147%2039.9238%2033.1051%2026.9985C23.4944%208.17586%2014.0767%201.32328%2014.0767%201.32328C17.285%20-1.64734%2041.451%20-0.788575%2059.229%2016.3692C67.5177%2024.3697%2067.2962%2023.3619%2079.8366%2044.0073V44.0161Z'%20fill='%23EF9920'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_882_3310'%3e%3crect%20width='136'%20height='136'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

What Is Longevity Risk?

Why Outliving Your Assets Is a Distinct Financial Risk — and the Strategies Designed to Address It

This article provides general information about retirement planning concepts and should not be considered personalized financial, legal, or tax advice. All strategies discussed involve trade-offs and risks that depend on individual circumstances.

Longevity risk is the risk that an individual will outlive their financial assets. It is not a risk of poor investment returns or poor financial decisions — it is the risk that even a well-funded, well-managed retirement will eventually run short of money because the retiree lives longer than the plan assumed.

The risk is specific, quantifiable, and often underestimated. Most people anchor their planning to average life expectancy, which, for a healthy 65-year-old American, is approximately 84–85 for men and 86–87 for women according to current actuarial data from the Social Security Administration. But average life expectancy is not the right planning horizon: it means roughly half the population lives longer than that age. A retiree who plans to 85 and lives to 94 has a nine-year funding gap. A couple where one spouse lives to 97 has an even larger one.

For high-income professionals who retire early — in their 50s or even late 40s — the planning horizon may extend to 40 or 50 years, far beyond what most financial planning models treat as a base case.

Why Life Expectancy Estimates Understate the Risk

The numbers that appear in actuarial tables and financial planning literature are period life expectancies — based on today's mortality rates across all age groups. They do not account for two important factors that tend to push the actual longevity of financially literate, high-income retirees above the average.

Survivorship: Life expectancy at birth incorporates early mortality — deaths in childhood, young adulthood, and middle age. A person who is already 65 and healthy has already survived those risks. The remaining life expectancy from age 65 is meaningfully longer than the figure implied by birth life expectancy.

Socioeconomic factors: Health outcomes and life expectancy are strongly correlated with income, education, and access to healthcare — all of which skew high for Nauma's core audience of tech workers and high-income professionals. A 65-year-old in excellent health in a high-income household has a significantly longer expected lifespan than the population average.

The joint life expectancy for couples adds another layer. For a married couple both age 65, there is approximately a 50% probability that at least one spouse lives past 90, and roughly a 25% probability that at least one lives past 95. These are not extreme tail scenarios — they are the base case for planning purposes for many couples.

The Cost of a Longer Retirement

Longevity risk is a financial risk because longer retirement creates larger cumulative spending needs. A retirement plan funded for 25 years at $100,000 per year of inflation-adjusted spending requires a significantly smaller initial portfolio than one funded for 35 years at the same spending level. Under a 4% withdrawal rate assumption, a 25-year plan requires approximately $1.6 million; a 35-year plan requires approximately $2.2 million — a 38% difference driven entirely by time horizon.

This calculation compounds when the additional years fall late in life, when healthcare and long-term care costs typically accelerate. The last decade of life is often the most expensive in healthcare terms — not necessarily in total spending if the retiree has reduced other discretionary spending, but certainly in terms of medical, nursing, and assisted living costs. See Long-Term Care for a full treatment of how to plan for these costs specifically.

Why Longevity Risk Is Different From Other Financial Risks

Most financial risks have natural hedges or mitigation strategies that do not require certainty about the future. Sequence of return risk can be managed through asset allocation and dynamic withdrawal. Inflation risk can be addressed through TIPS, real assets, and inflation-adjusted income. Investment risk can be reduced through diversification.

Longevity risk is different because it is, at its core, uncertainty about a single unknowable variable: how long you will live. No investment strategy, no portfolio allocation, and no withdrawal rule eliminates the possibility of living longer than the plan assumed. A retiree can run the best possible plan and still face funding shortfalls at 93 if they projected to 88.

This makes longevity risk the one risk in retirement planning that is most naturally addressed through insurance mechanisms — specifically, instruments that provide guaranteed income for life regardless of how long that life turns out to be. The insurance company bears the longevity risk on behalf of the policyholder, pooling it across many lives.

Commonly Discussed Approaches for Managing Longevity Risk

Delay Social Security to Maximize the Guaranteed Inflation-Adjusted Benefit

Social Security has several features that make it a meaningful longevity hedge. It is inflation-adjusted, backed by the federal government, and paid for life — no matter how long that life is. Under current law, every year of delay beyond full retirement age (up to age 70) increases the monthly benefit by approximately 8%. Delaying from age 67 to 70 increases the benefit by approximately 24% permanently, though Social Security rules are subject to legislative change.

For a retiree who lives to 95, the cumulative value of a larger Social Security benefit — both in dollars received and in longevity protection — is substantial. For a couple, the higher earner's Social Security decision is also the survivor benefit decision: the surviving spouse receives the higher of the two benefit amounts, so maximizing the higher earner's benefit is a direct longevity hedge for the surviving spouse. See When Should You Claim Social Security? for a full framework for the claiming decision.

Longevity Annuities (DIA and QLAC)

A deferred income annuity (DIA) is a contract in which the purchaser pays a premium today in exchange for a guaranteed income stream beginning at a specified future date — typically age 80 or 85. Unlike a single premium immediate annuity (SPIA), a DIA provides no income before the start date. If the purchaser dies before the start date, payments do not begin (unless a return-of-premium rider is included, at additional cost).

The efficiency of a DIA as longevity insurance lies in the mortality credits: premiums from purchasers who do not survive to the start date implicitly subsidize the payments of those who do. This pooling mechanism allows a relatively modest premium to generate substantial guaranteed income beginning at a late age. Hypothetical example for illustration only: a $150,000 DIA purchased at age 65 might generate $3,000–$4,500 per month beginning at age 85, though actual payout rates depend on the insurer, the purchaser's age and gender, and interest rate conditions at the time of purchase. Annuity contracts are also subject to counterparty risk — the financial strength of the issuing insurance company — and are generally illiquid once purchased.

A Qualified Longevity Annuity Contract (QLAC) is a specific form of DIA that can be purchased inside a traditional IRA or 401(k), with income beginning no later than age 85. Under IRS Notice 2025-67, the 2026 QLAC contribution limit is $210,000 per person (indexed for inflation annually), and those assets are excluded from Required Minimum Distribution calculations until income begins. This provides a dual benefit: longevity insurance and RMD deferral. Note that QLAC payments, when they begin, are taxed as ordinary income. See Annuities for the full explanation of DIA and QLAC structures, tax treatment, and trade-offs.

Lower the Withdrawal Rate

A lower initial withdrawal rate extends the sustainable life of the portfolio in historical simulations. A portfolio managed at a 3% withdrawal rate has survived essentially all historical 40-year periods in back-tested research, while a 4% rate shows more failure cases at longer horizons. For retirees with very long time horizons — particularly early retirees in their late 40s or 50s — the starting withdrawal rate is one of the primary variables that determines how long the portfolio can sustain withdrawals.

The cost of a lower withdrawal rate is reduced spending in earlier years. For a retiree with $3,000,000 in investable assets, the difference between 4% ($120,000 per year) and 3% ($90,000 per year) is meaningful. Whether the trade-off is appropriate depends on the full income picture: if Social Security and other guaranteed income already covers essential expenses, the portfolio withdrawal may fund only discretionary spending, in which case a lower rate on the discretionary portfolio is easier to sustain.

The Floor-and-Upside Framework

One framework frequently considered by retirement planning professionals is the floor-and-upside approach: securing guaranteed income sufficient to cover essential expenses for life (through Social Security, pensions, and potentially annuities), and managing the upside portfolio for long-term growth and discretionary spending. Longevity risk on the essential expense layer is transferred to guaranteed income sources; longevity risk on the discretionary layer is accepted but managed through investment discipline. See What Is the Floor-and-Upside Strategy? for a complete explanation of this framework.

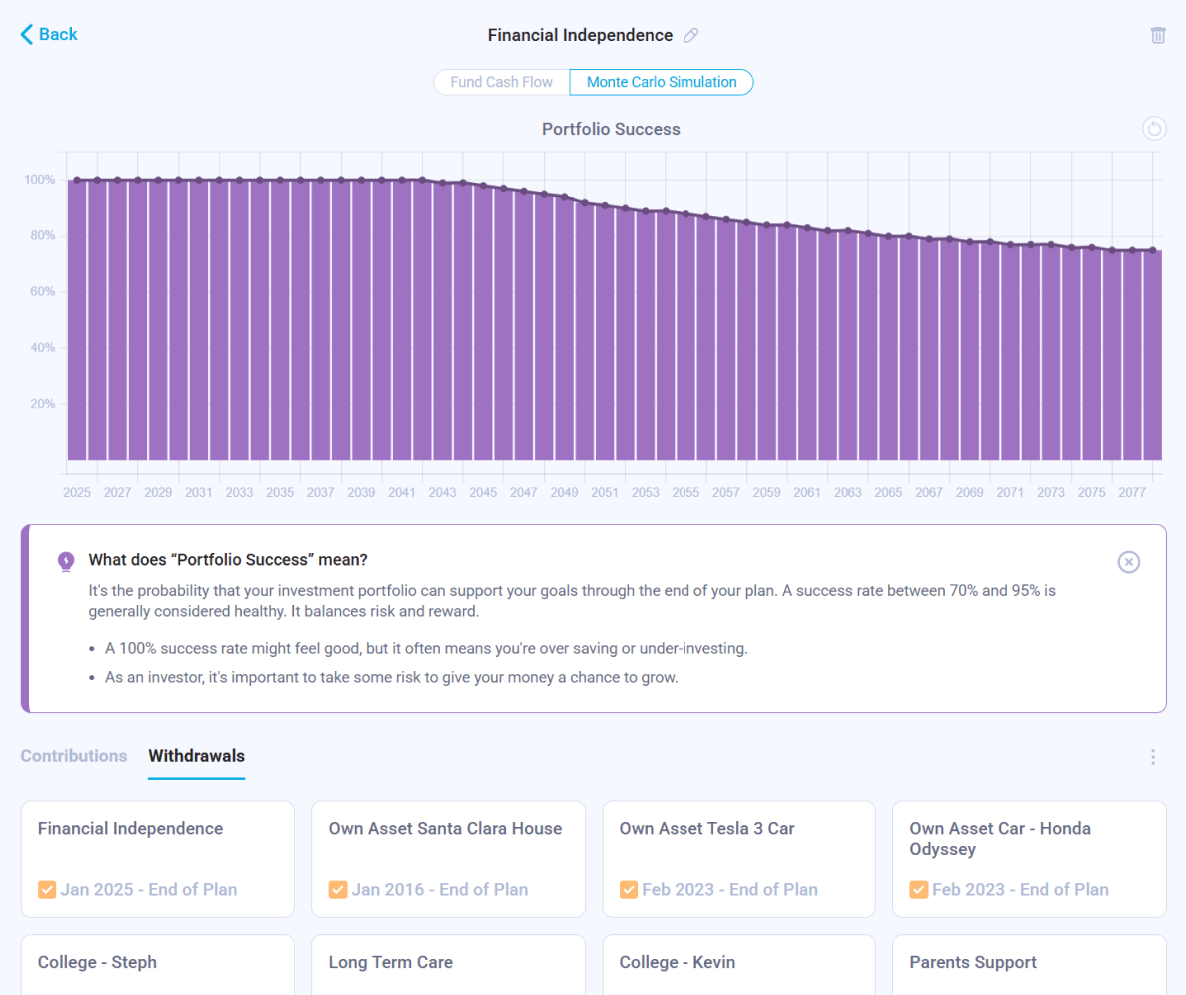

Monte Carlo Simulation for Long Horizons

Monte Carlo simulation — running the retirement plan through thousands of randomized market scenarios — is the standard tool for quantifying longevity risk in probabilistic terms. By extending the simulation to age 95 or 100 rather than a fixed planning horizon, the simulation captures the tail risk of a very long life. A plan with an 85% probability of success to age 90 but only a 60% probability to age 97 reveals a meaningful longevity risk gap even if the shorter-horizon picture looks fine. Monte Carlo results are model outputs based on statistical assumptions, not predictions of future market behavior. See What Is Monte Carlo Simulation? for how these simulations are structured and interpreted.

The Healthcare Wildcard

Any discussion of longevity risk is incomplete without acknowledging that longer life is not simply more years of current spending — it is more years with an increasing probability of healthcare needs, assisted living, and memory care. According to 2026 data, the national median cost of a private room in a nursing facility is approximately $376 per day, or around $135,000–$137,000 per year, with significant regional variation (California costs are substantially above the national median). Home health aide services average $30–$60 per hour depending on location and service level.

A retiree who lives to 95 with five years of assisted living or nursing care needs faces healthcare costs alone of $400,000–$700,000 at current prices — before inflation — on top of all other retirement expenses. Long-term care insurance and hybrid life/LTC products exist specifically to address this risk. See Long-Term Care for a full treatment of coverage options and planning considerations.

This article is for educational purposes only and does not constitute investment, tax, or financial advice. Life expectancy projections are statistical estimates and do not apply to any specific individual. QLAC limits and RMD rules reflect current US law as of 2026 (IRS Notice 2025-67 and SECURE 2.0 Act) and are subject to future legislative change. Annuity payout rates depend on insurer terms, the purchaser's age and health, and market conditions at the time of purchase; annuities carry counterparty risk and are generally illiquid once purchased. Nursing home cost figures reflect 2026 national median data and vary significantly by region. Social Security projections are subject to legislative change. Always consult a qualified financial advisor before making retirement income decisions.

Frequently Asked Questions

Stress-Test Your Plan to Age 95 and Beyond

Nauma's Monte Carlo simulation lets you extend your retirement projection to any age — so you can see exactly how longevity risk affects your probability of success and what changes most improve the long-horizon outcome.

Get Started for Free